Managing business finances manually is slow, error-prone, and time-consuming. Missed invoices, delayed payments, and hours spent on financial reports can hinder growth.

What if financial reports updated themselves and payments were always accounted for?

Accounting automation eliminates repetitive tasks like data entry, invoice processing, and reconciliations. With real-time reporting and easy integrations, businesses can cut costs, improve accuracy, and make faster financial decisions.

Before exploring how to automate accounting, let’s first compare manual versus automated accounting to understand the key differences.

Manual accounting (Traditional) vs Automated accounting

| Manual accounting | Automated accounting | |

| Data entry | Requires manual input which increases the risk of human errors. | Automates data imports from invoices, receipts, and bank statements. |

| Invoice processing | Invoices are created, sent, and tracked manually, which can lead to delays. | Generates and sends invoices automatically with reminders for overdue payments. |

| Payment tracking | Requires manual reconciliation with bank statements. | Payments are automatically recorded and matched with transactions. |

| Financial reporting | Manual reports are often outdated by the time they are completed. | Real-time reports update automatically and provide up-to-date insights. |

| Time & cost | Labor-intensive. Requires more staff and higher costs. | Saves time and reduces operational expenses. |

| Scalability | Difficult to scale as the business grows. | Scales easily with increasing financial data. |

What accounting processes can be automated?

Accounting involves multiple processes, from tracking revenue and expenses to managing payroll and tax compliance. Automation helps you streamline these tasks while maintaining accuracy and efficiency. It also provides better financial insights for businesses to plan, forecast, and make informed decisions with up-to-date data.

Below are some common accounting processes, their challenges, and how automation can help.

Financial accounting automation

Financial accounting tracks a company’s overall financial health, including cash flow, profit and loss, and balance sheets. Financial accounting tools simplify this process by consolidating financial data, categorizing transactions, and generating structured reports.

Revenue accounting automation

Tracking income, managing customer payments, and accurately recognizing revenue is essential for financial stability. Automated revenue tools allow businesses to monitor cash flow more effectively, minimize errors, and gain better insights into their earnings.

Accounts payable automation (AP)

Processing vendor invoices manually involves tracking due dates, verifying amounts, and making payments. This often leads to missed deadlines or duplicate payments. AP tools can auto-match invoices with purchase orders, schedule payments, and send alerts for upcoming due dates.

Accounts receivable automation (AR)

Chasing overdue invoices takes time, and human errors in payment records can lead to disputes or cash flow gaps. AR automation sends invoices automatically, follows up with reminders, and reconciles payments with bank transactions.

Payroll accounting automation

Manually tracking salaries, deductions, and tax filings is complex and increases the risk of miscalculations. Payroll software calculates salaries, deducts taxes, and ensures compliance with labor laws, therby reducing payroll errors.

Invoice accounting automation

Managing and reconciling invoices manually leads to inefficiencies, delays, and errors. Invoice automation ensures seamless tracking, categorization, and integration with accounting tools.

Tax accounting automation

Keeping up with changes in tax law and calculating tax liabilities requires constant monitoring and manual adjustments. Tax software auto-updates tax rates, calculates taxes accurately, and generates compliance-ready reports.

How to automate accounting process

Switching from manual accounting to automation doesn’t happen overnight. Businesses need a structured approach to ensure a smooth transition without disrupting daily operations. The key is to start small, choose the right accounting automation tools, and gradually scale automation.

Here’s how to automate the accounting process step by step.

Step 1 – Identify areas of automation

Not every accounting task needs automation right away. The first step is to assess your current financial workflows and pinpoint processes slowing down efficiency, prone to errors, or requiring repetitive manual input.

Start by asking these key questions:

- Which accounting tasks consume the most time and effort?

- Where do human errors frequently occur (e.g., data entry, reconciliation, or invoicing)?

- Are there any compliance-related tasks that could benefit from automation?

- Which financial processes require frequent updates or real-time tracking?

Some of the most common areas for automation include invoice management, payment reconciliation, payroll processing, tax calculations, and financial reporting.

By first identifying the most inefficient and error-prone tasks, you can prioritize automation efforts that will have the greatest impact on productivity, accuracy, and cost savings.

Once you have a clear list of processes to automate, the next step is to select the right tools to integrate with your existing accounting system and gradually implement automation.

Step 2 – Select the accounting automation tools

Once you know which processes to automate, the next step is choosing the right tools. The right accounting automation software should integrate well with your existing systems, reduce manual effort, scale as your business grows, and fit into your budget.

Below are different categories of accounting automation tools:

- Accounts payable & accounts receivable tools – Bill.com, Melio, HighRadius, AvidXchange, Tipalti

- Payroll automation tools – Gusto, ADP, Paychex, Deel, Rippling, Clockify

- Expense management tools – Expensify, Ramp, Spendesk, Emburse, Brex

- Tax accounting tools – Avalara, Vertex, TaxJar, Drake Tax, TurboTax Business

- All-in-one accounting tools – QuickBooks, Xero, Zoho Books, NetSuite, Sage Intacct

- Reporting automation & BI tools – Coupler.io, Looker Studio, Power BI, Tableau

Step 3 – Start with a single accounting process automation

The best way to implement accounting automation is to start with one process, successfully automate it, and expand from there. Let’s take an example.

A SaaS company struggling with manual data collection and reporting delays wants to automate invoice and payment tracking. They use:

- QuickBooks for invoice generation, financial statements, and tax reporting.

- Stripe for collecting subscription payments.

Instead of manually exporting and combining data, the company chose Coupler.io to automate the reporting process. This platform allows businesses to collect, transform, and visualize financial data, providing insights automatically.

Here’s how they used Coupler.io to automate invoice and payment tracking:

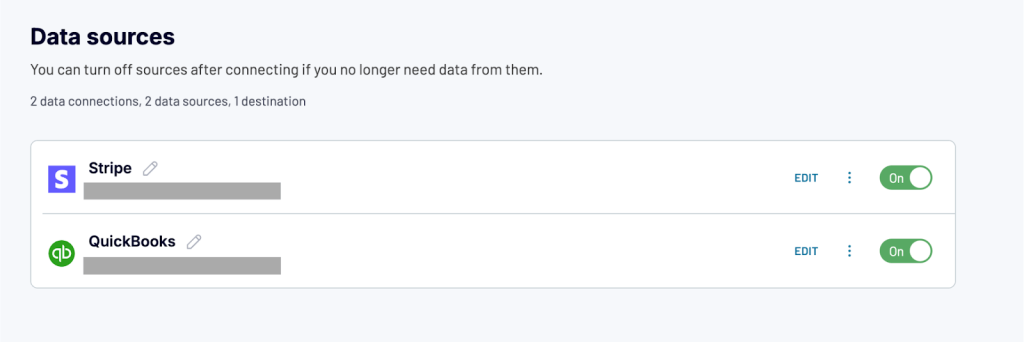

Connect multiple data sources

They connected QuickBooks and Stripe accounts using Coupler.io data flow. You can also add more sources in a single data flow. Coupler.io supports over 60 data sources, providing flexibility to scale their reporting setup as their business expands.

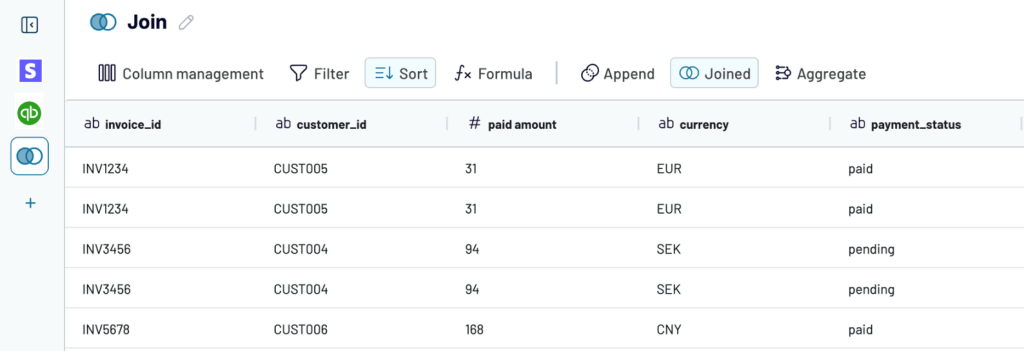

Transform data

Coupler.io offers built-in transformation options to organize your data in meaningful reports. In this example, they:

- Used the Join function to combine QuickBooks invoice data with Stripe payment transactions.

- Reconciled QuickBooks invoices with Stripe payments by adding a custom column called ‘Payment Reconciliation’ using a logical formula:

If the invoice amount = Stripe payment amount ? marked as “Paid.”

If the invoice amount > Stripe payment amount ? marked as “Payment Pending.”

- Included only essential data points like invoice status, dates, customer names, and outstanding balances to simplify reporting.

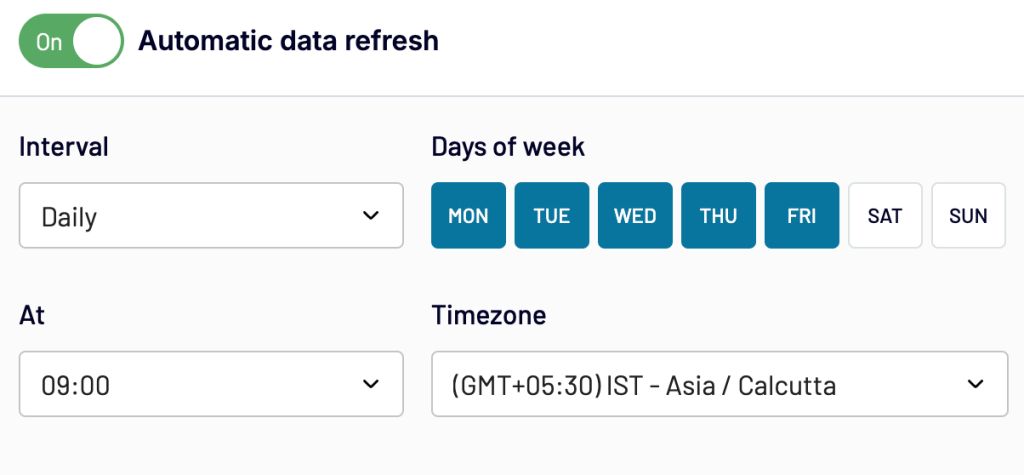

Load reports to BI tools and schedule data refresh

The report is transferred to Looker Studio for further data visualization. At the same time, Coupler.io also supports other BI tools, spreadsheets, and data warehouses as destinations for your data.

In Looker Studio, the SaaS company created a customized invoice and payment tracking dashboard that:

- Displays the total value of invoices issued and payments received.

- Tracks fluctuations in revenue over time.

- Shows the proportion of invoices that are fully paid vs. outstanding.

- Lists customers with unpaid invoices, including outstanding amounts.

Coupler.io updates this data automatically based on a set schedule so the dashboard remains accurate without manual updates.

Scheduled data refreshes allowed the SaaS company to monitor its financial performance frequently throughout the week. The real-time reporting by Coupler.io helped the finance team quickly identify overdue payments, track revenue accurately, and manage cash flow proactively. This timely insight improved collections and allowed for faster, informed financial decisions.

While this example focuses on integrating QuickBooks and Stripe, Coupler.io enables businesses to go beyond accounting data by combining financial information with CRM apps, project management tools, and other business systems.

For example, Project Alfred, an accounting firm, streamlined its financial reporting by connecting Xero with HubSpot and automatically loading data into Google Sheets. The result? They eliminated manual data transfers, cut reporting time, and saved 40 hours per month, which is equivalent to a full-time employee’s workload.

Curious how they achieved this? Check out the case study to see how automation transformed their finance operations.

If you are also looking for custom solutions to automate your accounting process, book a call with Coupler.io data experts.

Dashboard templates for accounting reporting automation

Accounting automation goes beyond eliminating manual data entry for your reports. It transforms how businesses track, analyze, and act on financial data. However,setting up reports from scratch can be time-consuming.

Use Coupler.io’s self-updating accounting dashboard templates to automatically visualize financial data from QuickBooks, Xero, Stripe, and more. This saves hours on manual reporting and enables faster business decisions.

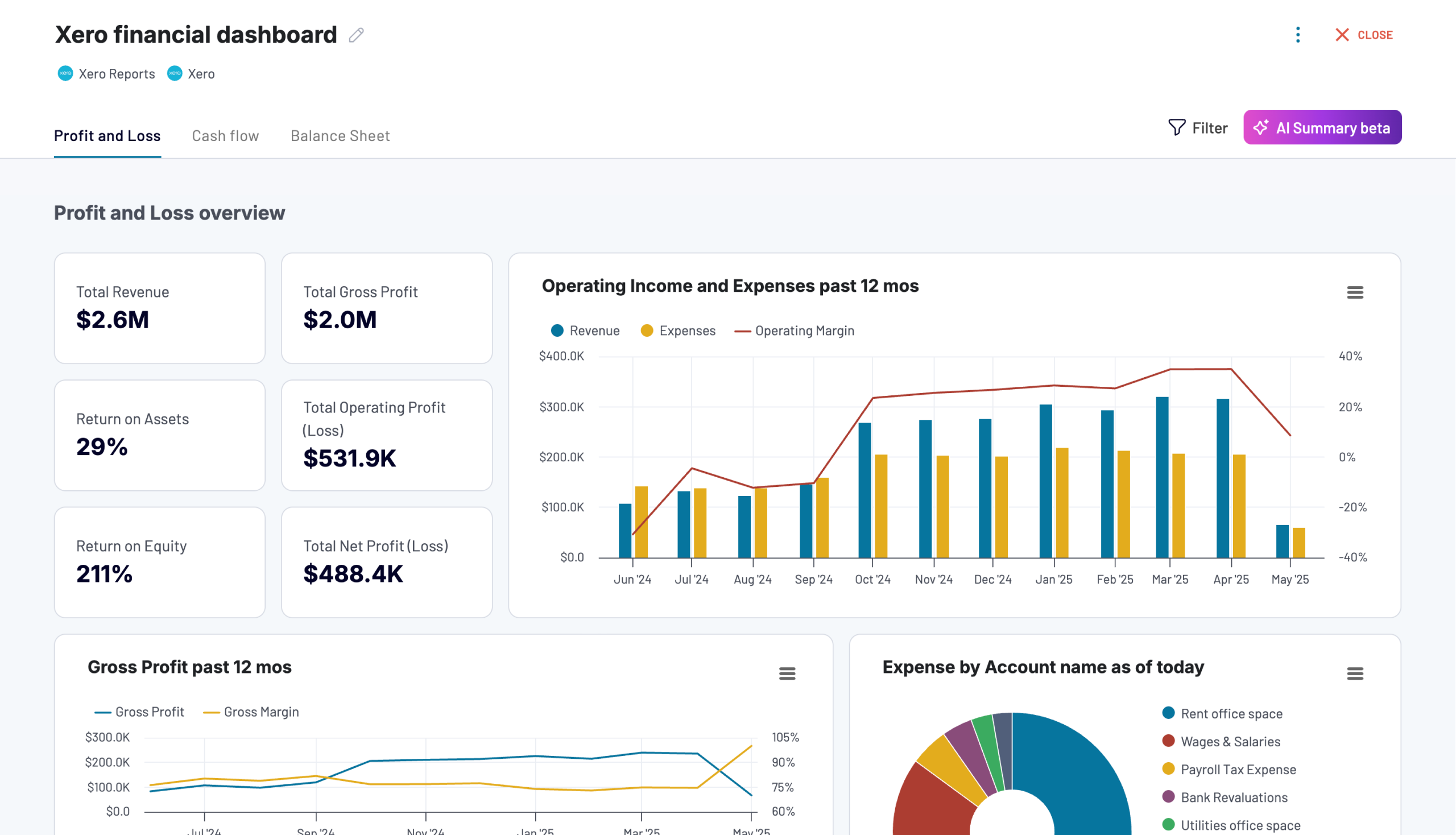

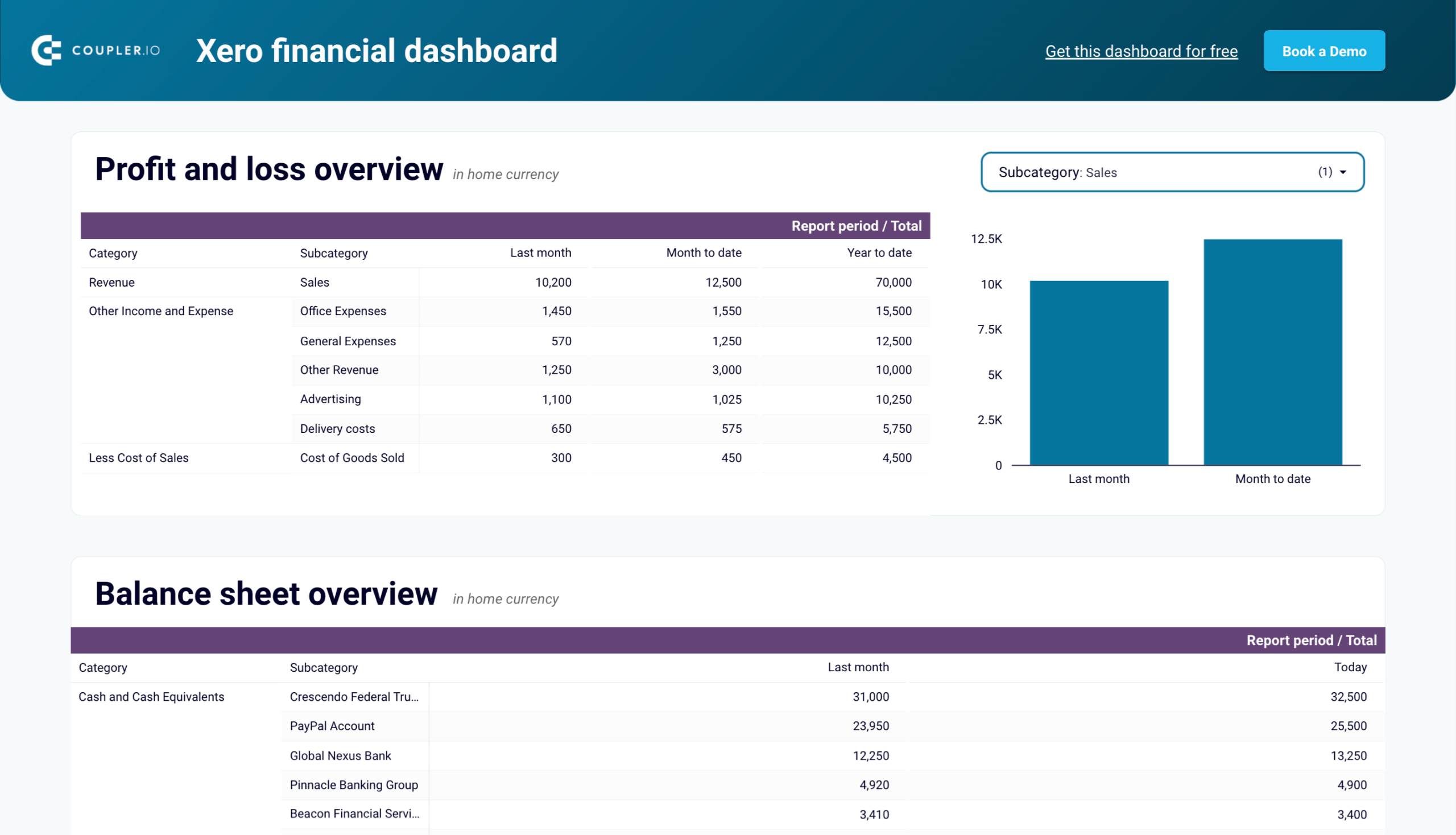

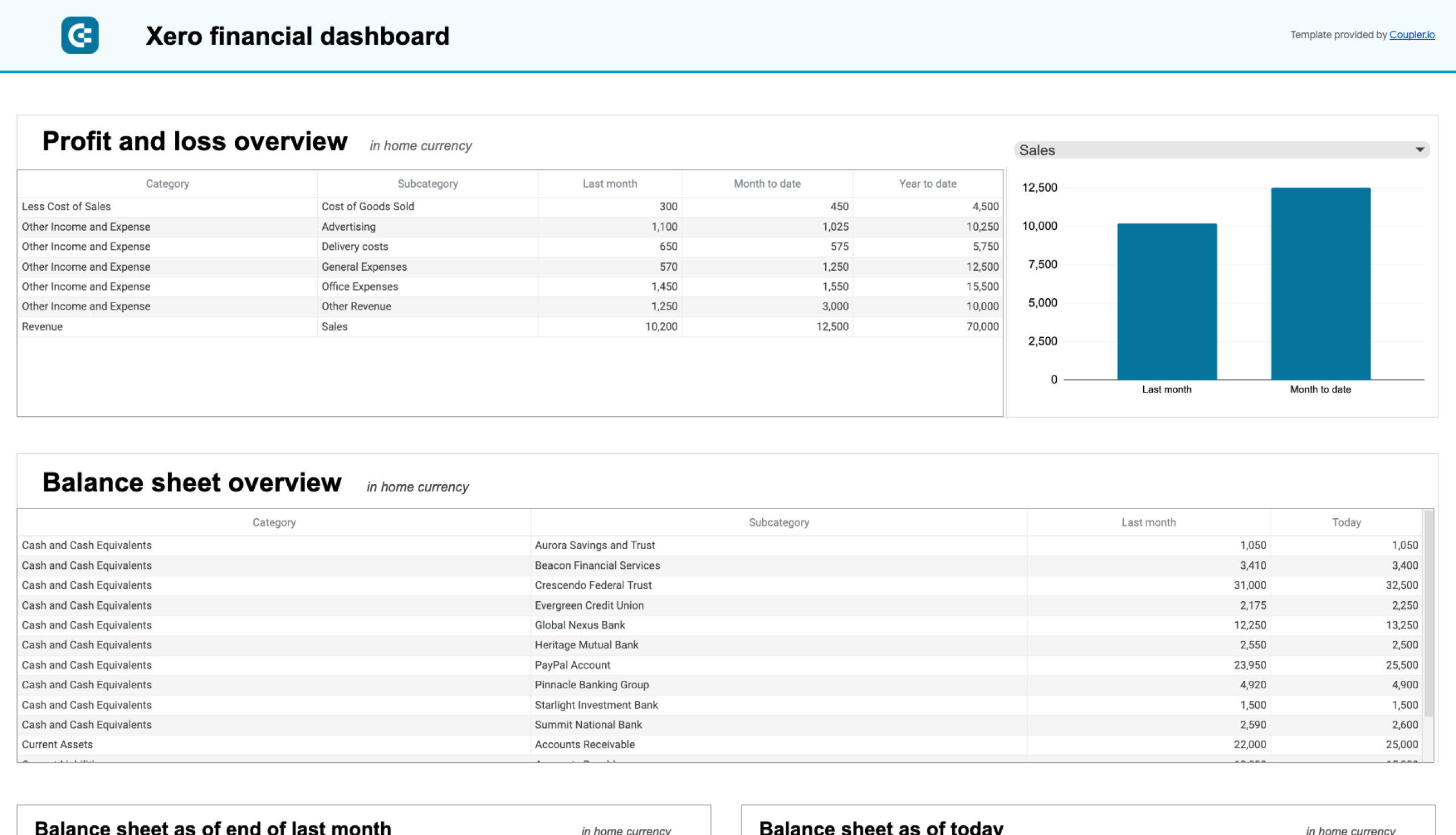

Xero financial dashboard

The Xero financial dashboard simplifies financial tracking for Xero users by automating profit and loss, cash flow, and balance sheet reports in real time.

This dashboard allows you to:

- Track profit & loss: View total revenue, operating expenses, and net income without manual calculations.

- Automate balance sheet updates: Get a real-time view of cash, liabilities, and equity for better decision-making.

- Monitor cash flow: See bank balances, net cash movements, and liquidity trends at a glance.

- Analyze revenue streams: Filter income sources by sales category, expenses, or cost of goods sold (COGS) to understand profitability.

You can use the dashboard in Coupler.io, which offers the AI insights feature designed to help you quickly make sense of your data. It is also available as a template in Looker Studio and Google Sheets. Connect your Xero account using the Coupler.io connector and follow the instructions in the Readme tab to set up the dashboard with your data.

Xero financial dashboard

Get comprehensive financial insights from your Xero account with key performance metrics, balance sheet analysis, and cash flow projections. Quickly assess your business health and make informed financial decisions.

Xero financial dashboard in Looker Studio

Analyze your financial performance with a unified dashboard featuring key reports from Xero like cash flow, profit and loss, balance sheet, and others.

Xero financial dashboard in Google Sheets

Get instant visibility into your company’s financial health through key performance reports from Xero such as cash flow, income statement, and balance sheet.

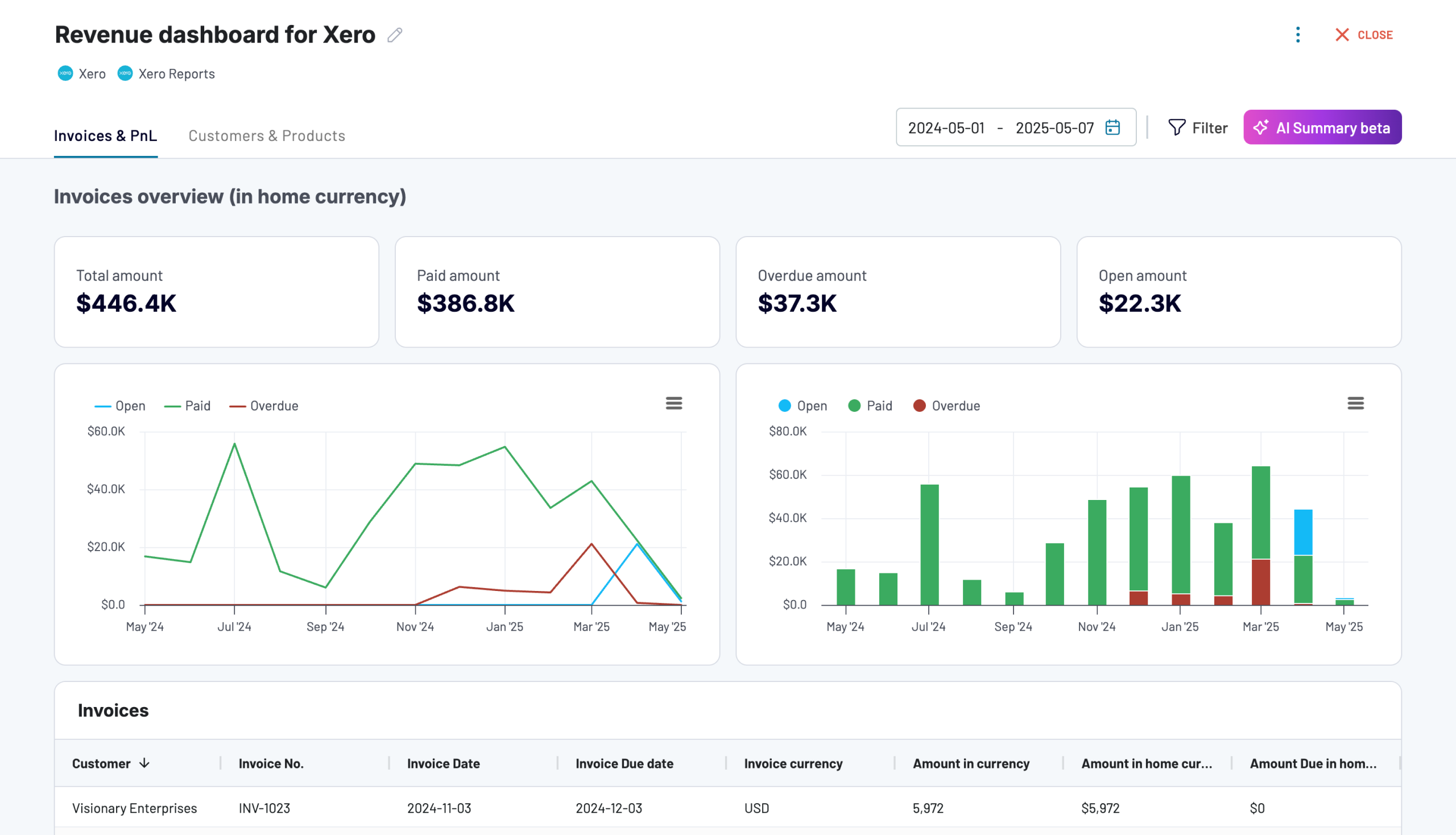

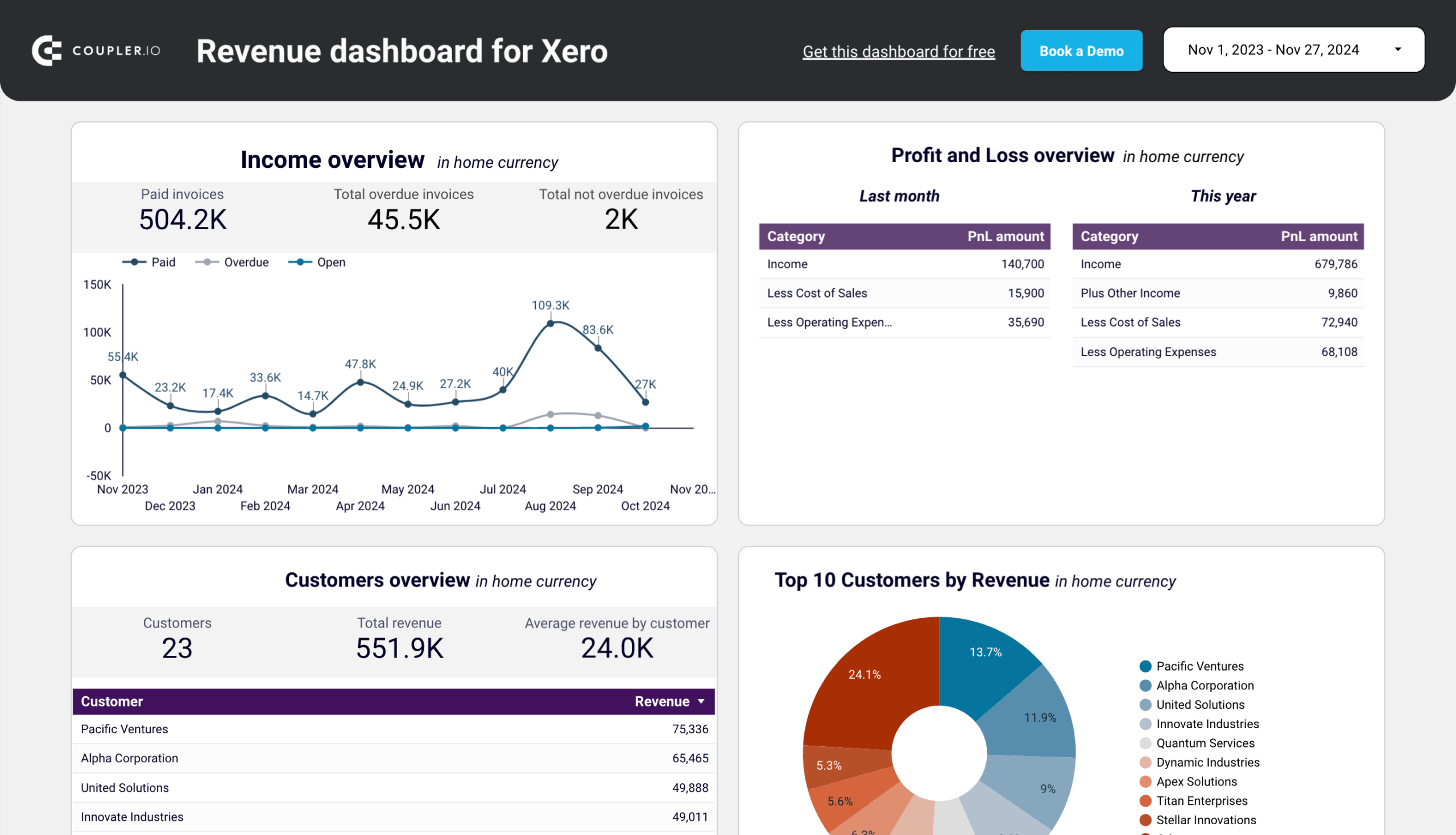

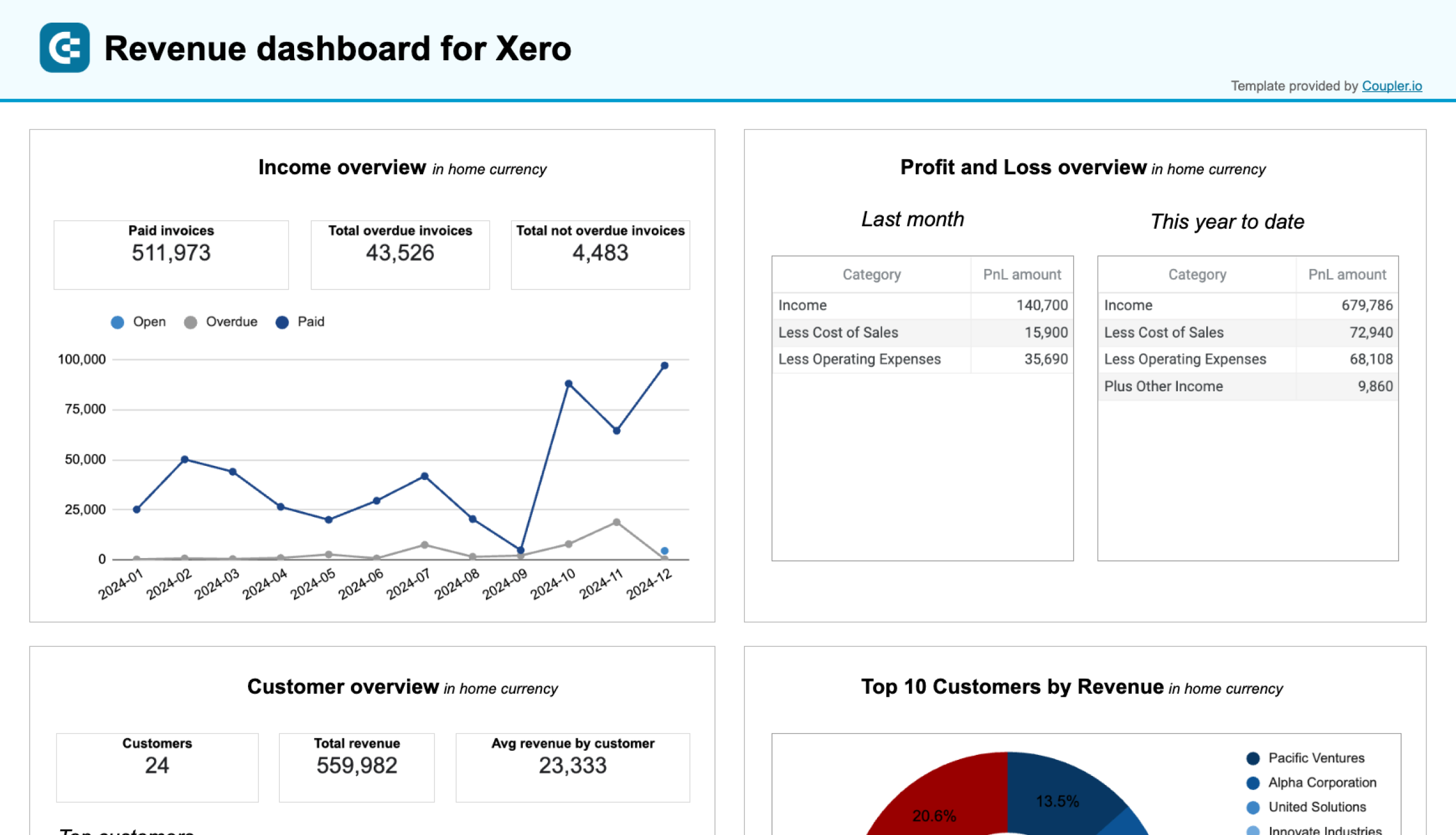

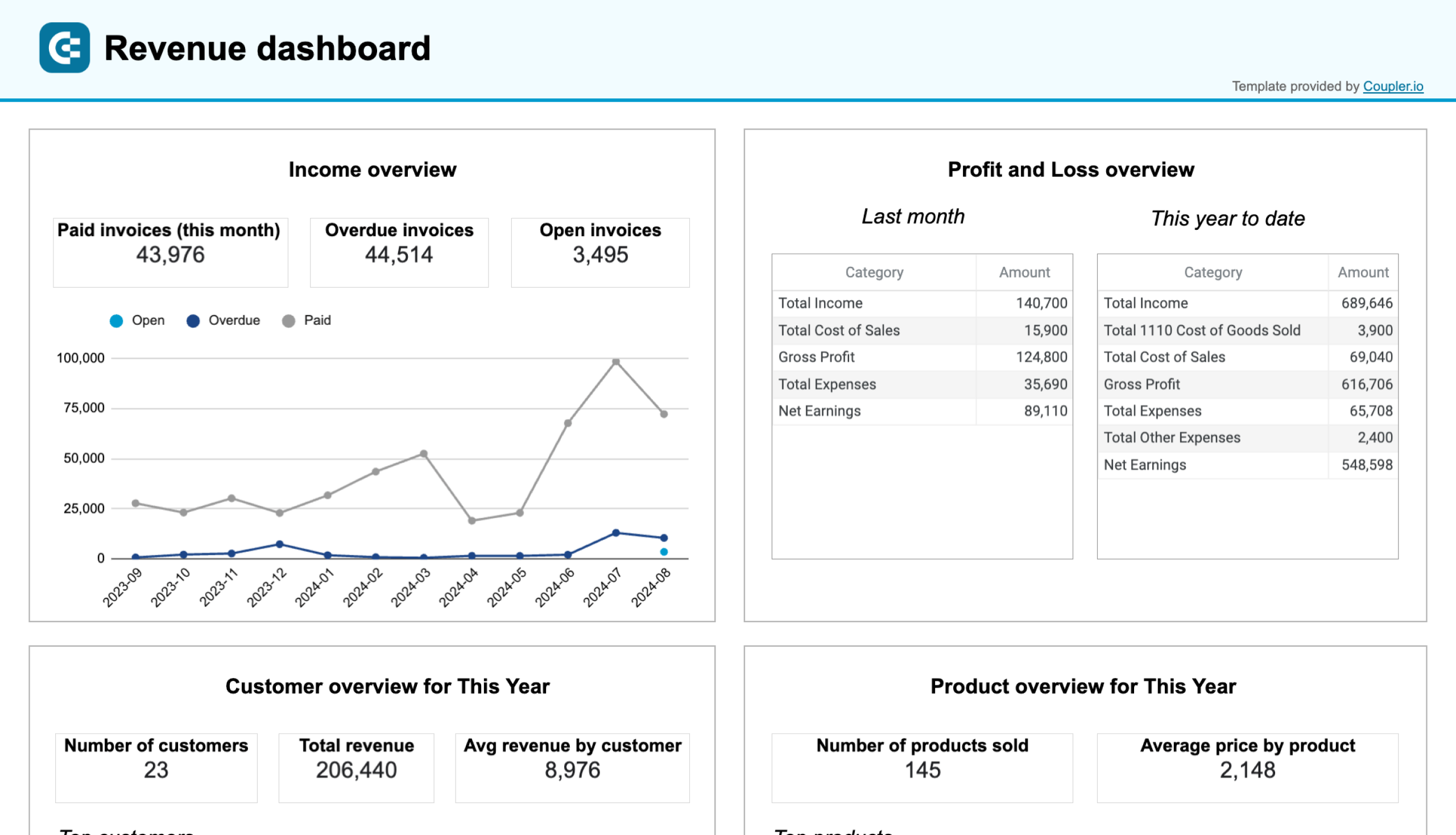

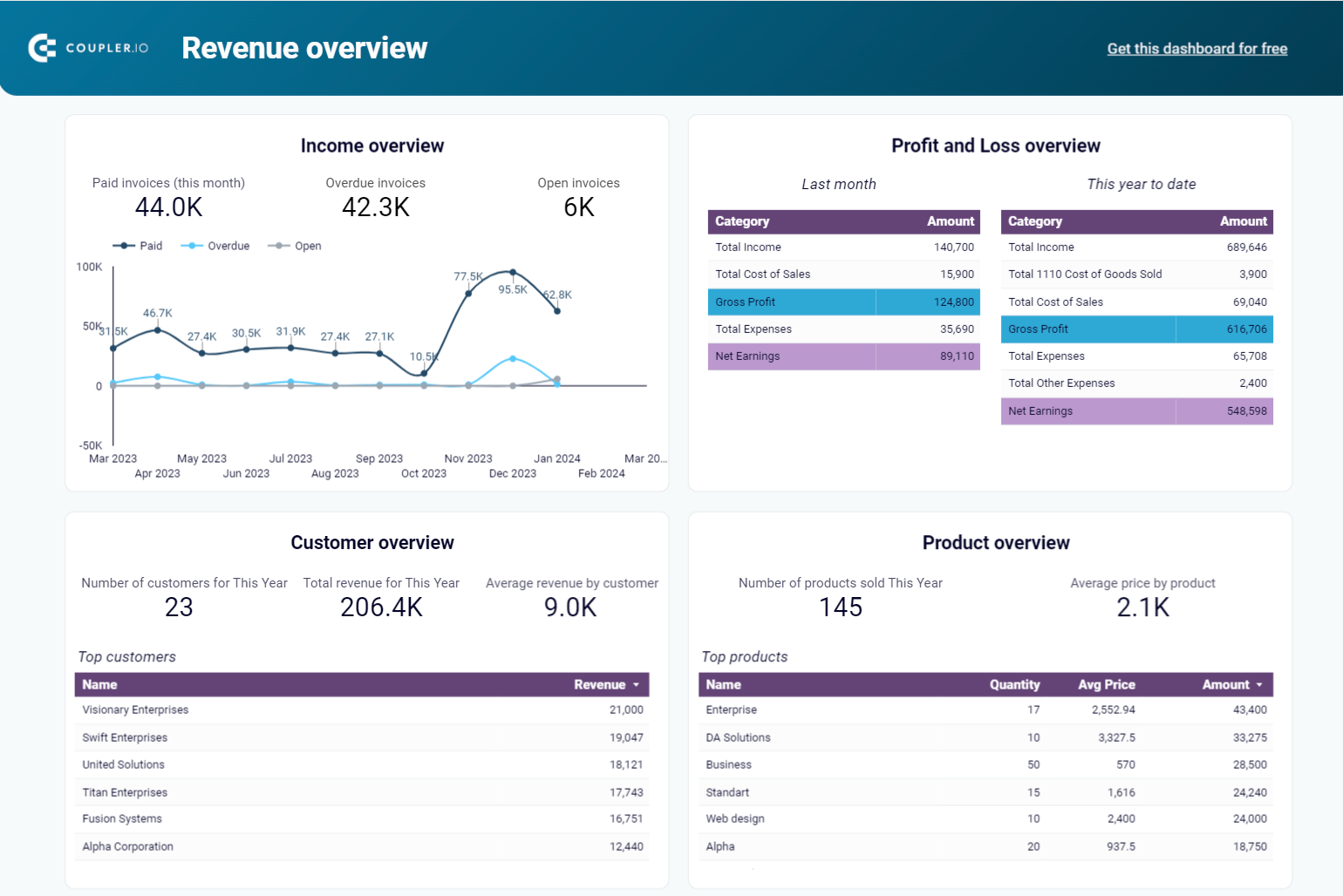

Revenue dashboard for Xero

The Xero revenue dashboard provides a clear view of a company’s revenue distribution, customer payments, and product sales trends. It automates revenue tracking, reducing manual data entry and reporting errors.

This dashboard allows you to:

- Track revenue growth: Monitor income fluctuations over time and adjust sales strategies accordingly.

- Evaluate profit & loss: Get a structured view of total revenue, expenses, and net earnings.

- Spot high-value customers: Identify the top contributors to revenue for better relationship management.

- Analyze product performance: See which products drive the most sales, supporting business growth decisions.

- View key revenue drivers: Displays the Top 10 Customers & Products by Revenue in a simple format.

This Coupler.io dashboard is available in Coupler.io and as a Looker Studio and Google Sheets template with a built-in Xero connector. To integrate it with your data, connect your Xero account using the Coupler.io connector and follow the instructions in the Readme tab.

Revenue dashboard for Xero

Analyze revenue streams, customer spending patterns, and product performance with data automatically synced from Xero. Gain actionable insights into sales trends, top-performing products, and high-value customers to drive growth strategies.

Revenue dashboard for Xero in Looker Studio

Get an overview of your profit and loss, products, and customers through a set of reports collected from Xero.

Revenue dashboard for Xero in Google Sheets

Track your revenue, costs, and customer insights with a comprehensive dashboard connected to your Xero account.

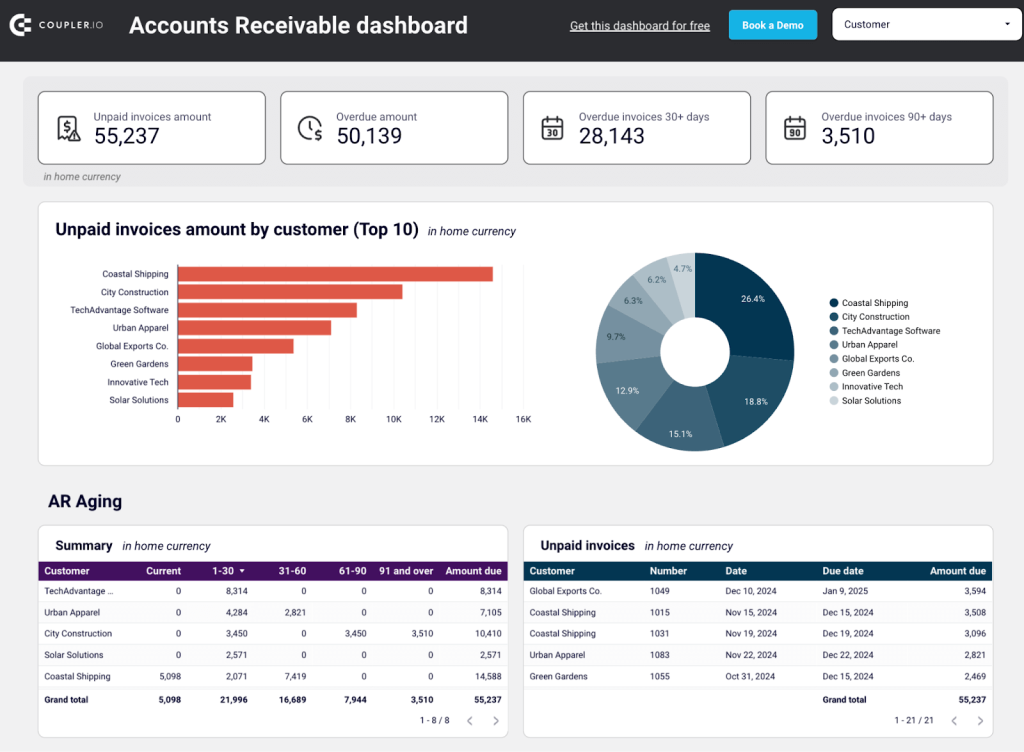

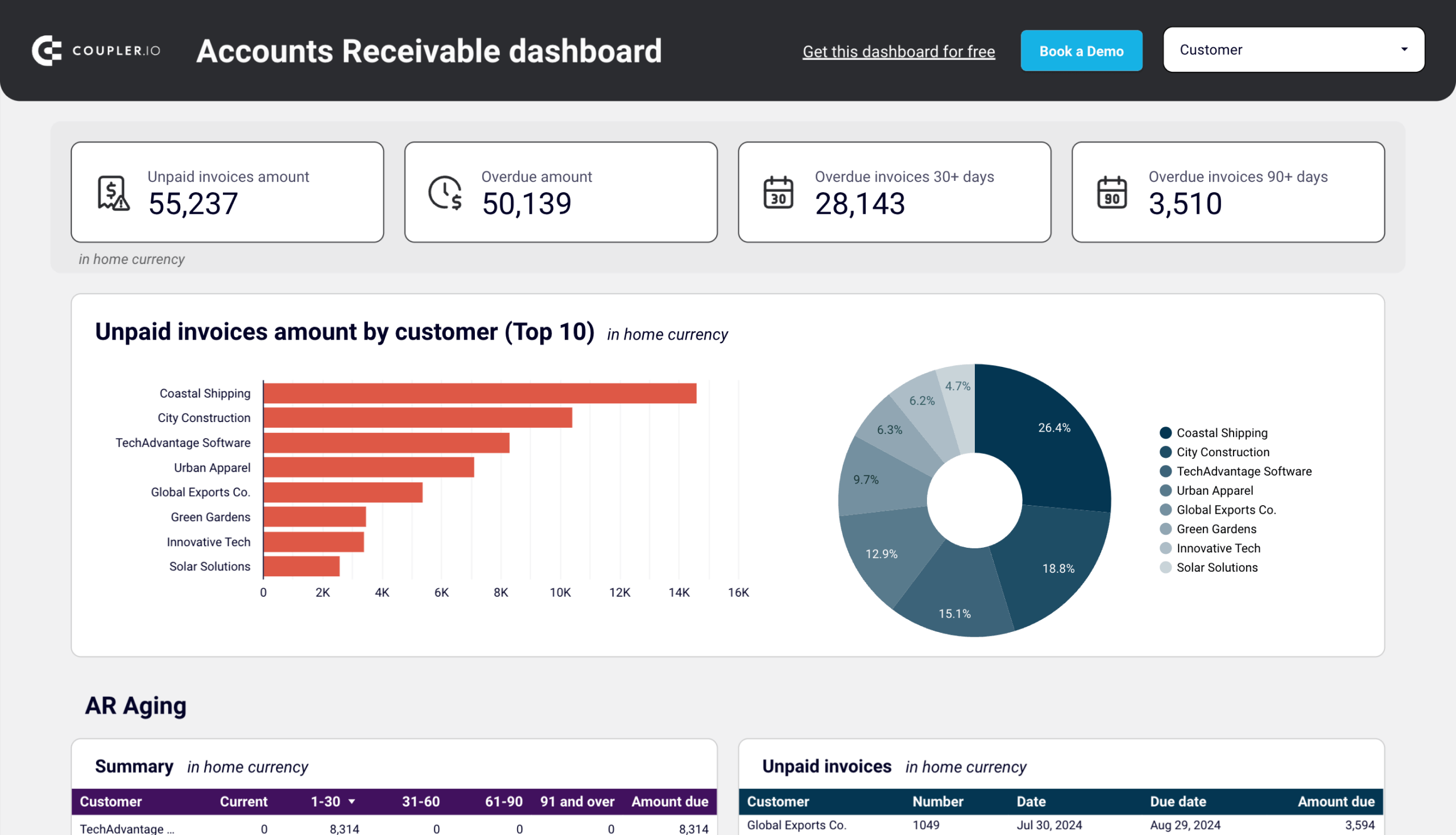

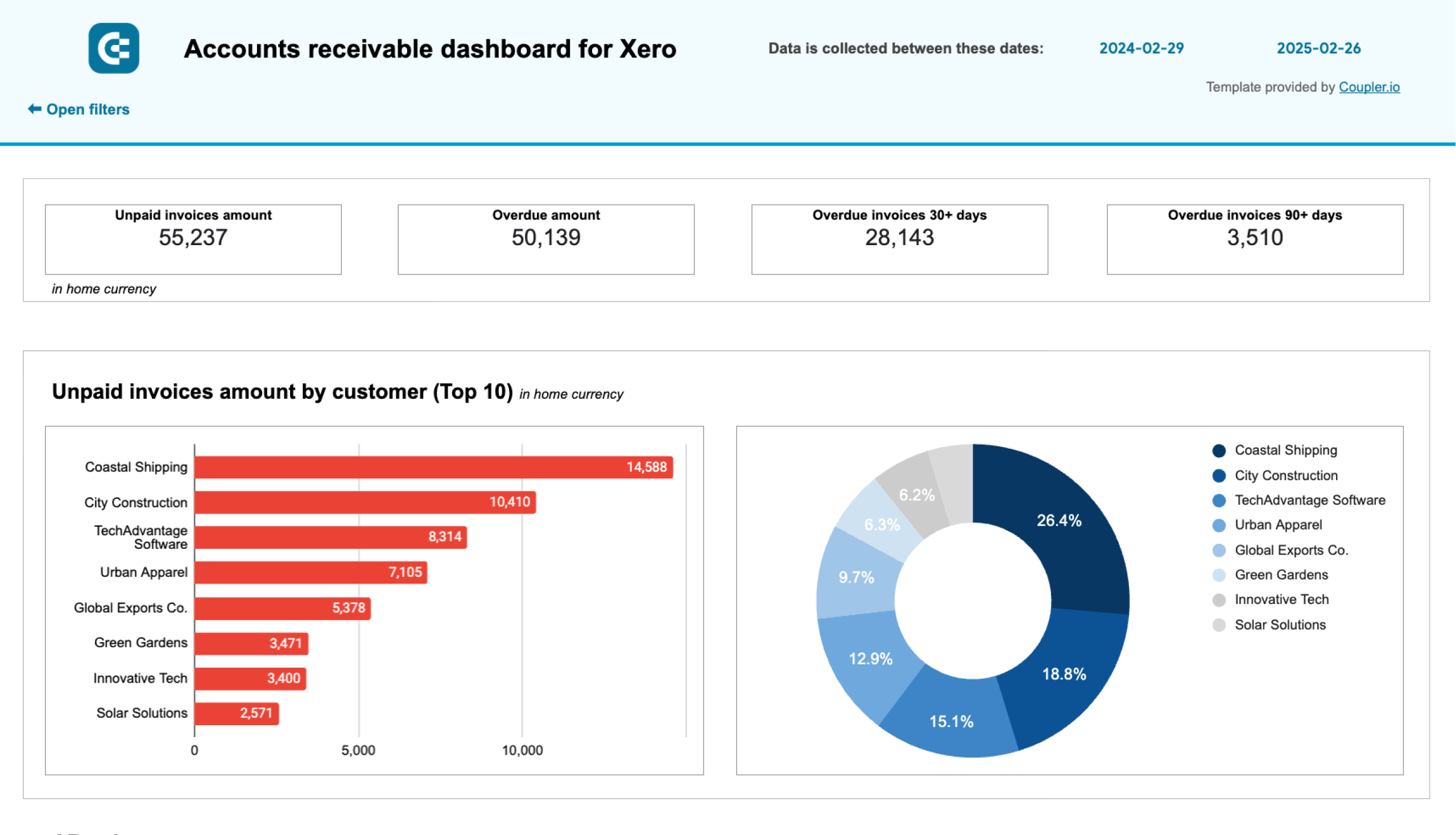

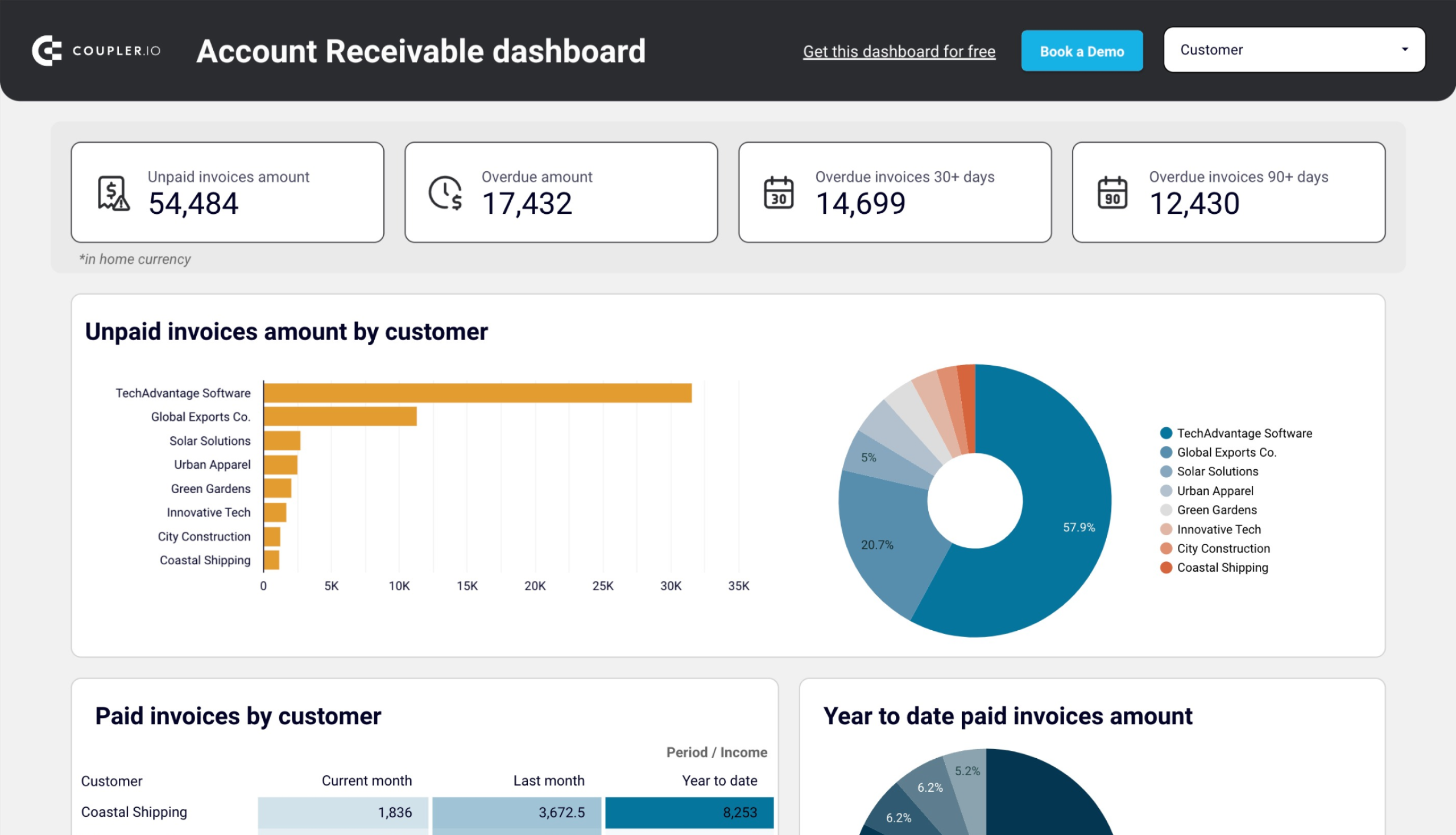

Accounts receivable dashboard for Xero

This dashboard makes managing receivables in Xero easier by consolidating key payment insights. It helps you monitor overdue payments, identify slow-paying customers, and track invoice collections without manual effort.

With this dashboard, you can:

- Outstanding receivables overview: Instantly see overdue invoice amounts and categorize them by due date.

- Customer payment patterns: Analyze who pays on time and which accounts require more follow-ups.

- Cash inflow trends: Review how receivables impact monthly cash flow.

- Aging invoice distribution: Get detailed insights into invoices pending for 30, 60, or 90+ days.

- Comprehensive invoice tracking: Access a complete list of invoices across multiple customers and currencies.

This dashboard is built in Looker Studio and Google Sheets. To integrate this dashboard with your data, connect your Xero account using the Coupler.io connector and follow the Readme tab for setup.

Accounts receivable dashboard for Xero in Looker Studio

See which customers accumulate unpaid and overdue invoices, analyze AR aging, and track changes over time.

Accounts receivable dashboard for Xero in Google Sheets

Track outstanding customer payments, monitor aging receivables, and analyze the correlation between paid and unpaid invoices to improve cash flow management.

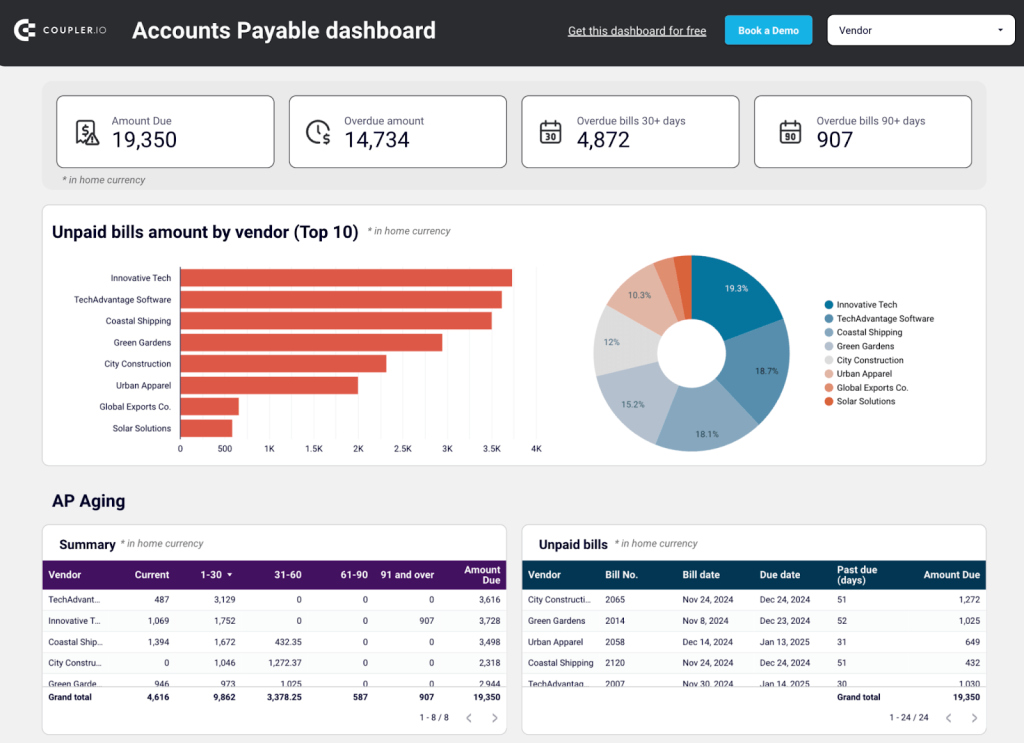

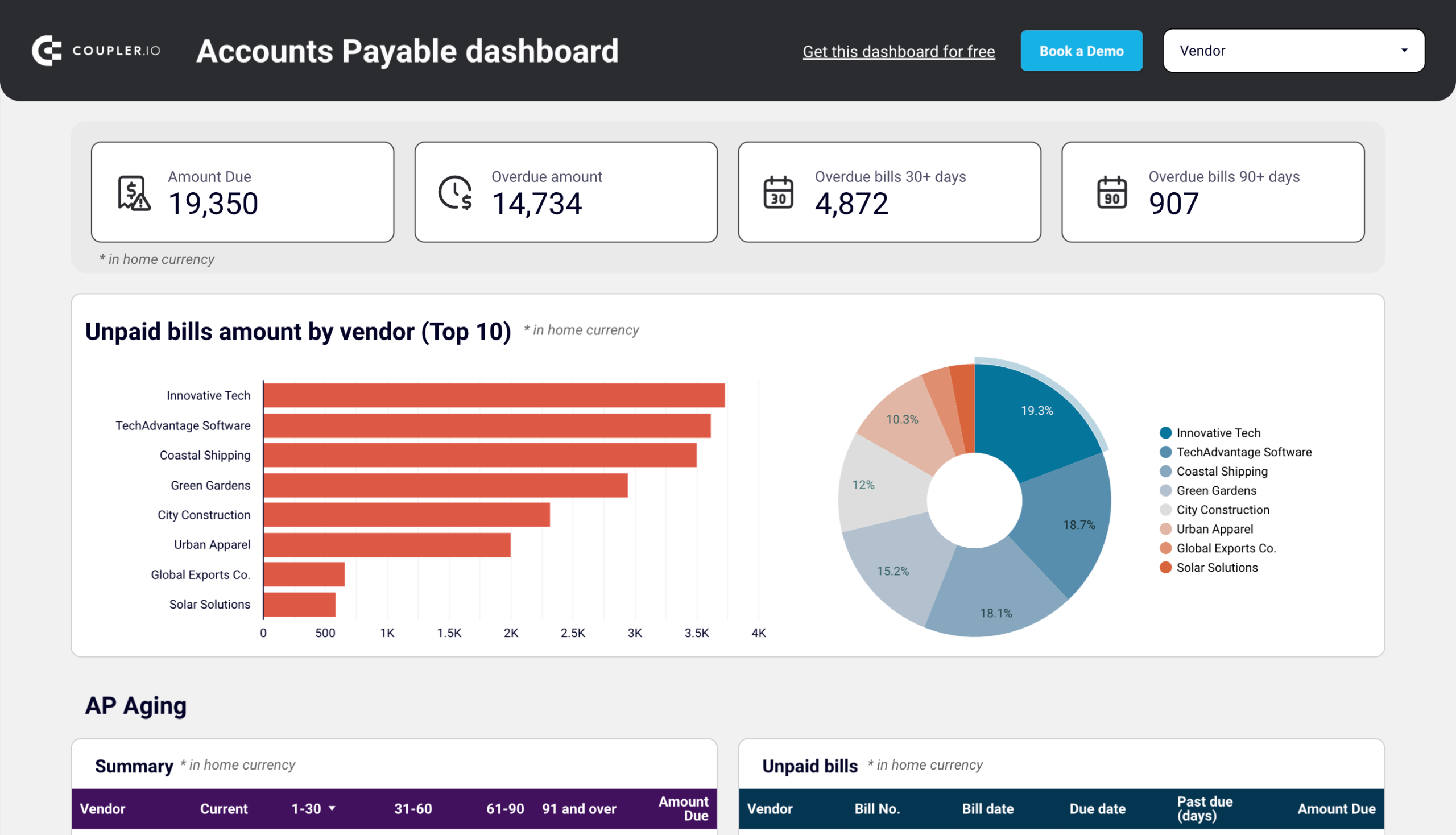

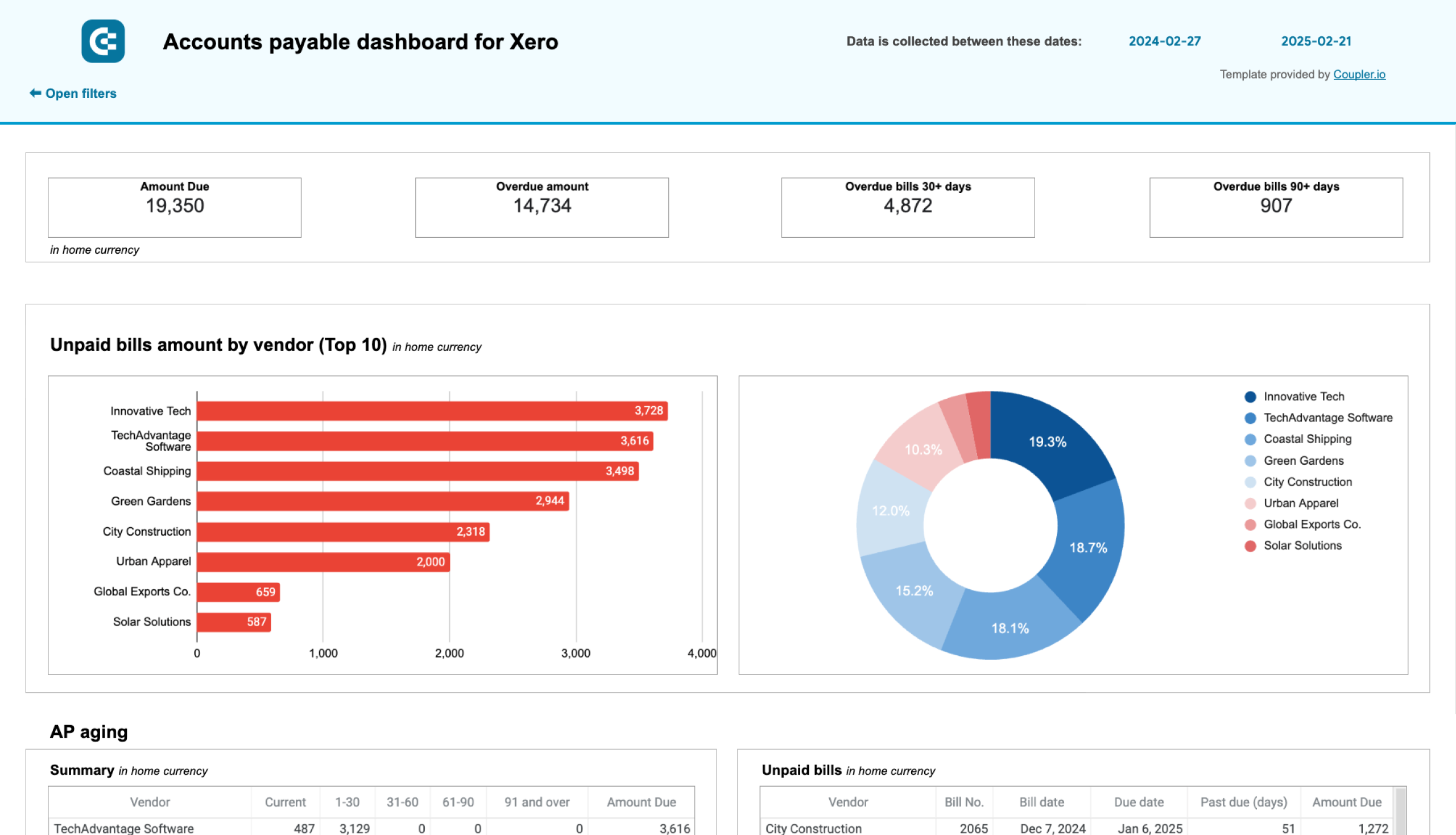

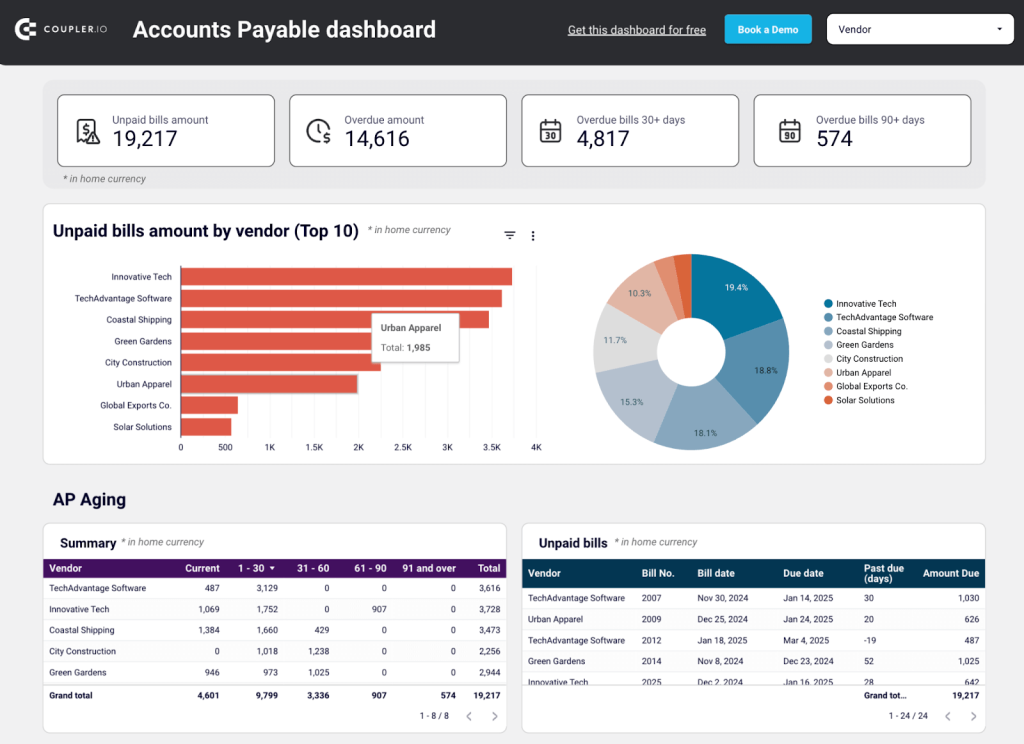

Accounts payable dashboard for Xero

This dashboard provides a real-time breakdown of outstanding vendor payments for Xero users to manage obligations efficiently.

With this dashboard, you’ll get:

- Instant visibility into outstanding payables: A single view of all unpaid invoices, overdue amounts, and upcoming due dates.

- Vendor-specific insights: Spot the vendors with the highest outstanding bills and prioritize payments accordingly.

- Aging schedule: Organizes overdue amounts into categories (current, 30+, 60+, 90+ days) to streamline payment decisions.

- Tracking of paid invoices: See historical payments by vendor to evaluate spending trends.

- Bank balance comparison: Assess available funds before making payments to avoid liquidity issues.

To integrate this Looker Studio dashboard with your data, connect your Xero account using the Coupler.io connector and follow the instructions in the Readme tab. You can also try the Google Sheets version of this template.

Accounts payable dashboard for Xero in Looker Studio

Track outstanding, overdue, and paid bills to optimize payment schedules, manage vendor relationships, and ensure smooth cash flow.

Accounts payable dashboard for Xero in Google Sheets

Monitor vendor payment deadlines, track aging bills, and analyze payment history to optimize cash flow management and maintain healthy supplier relationships.

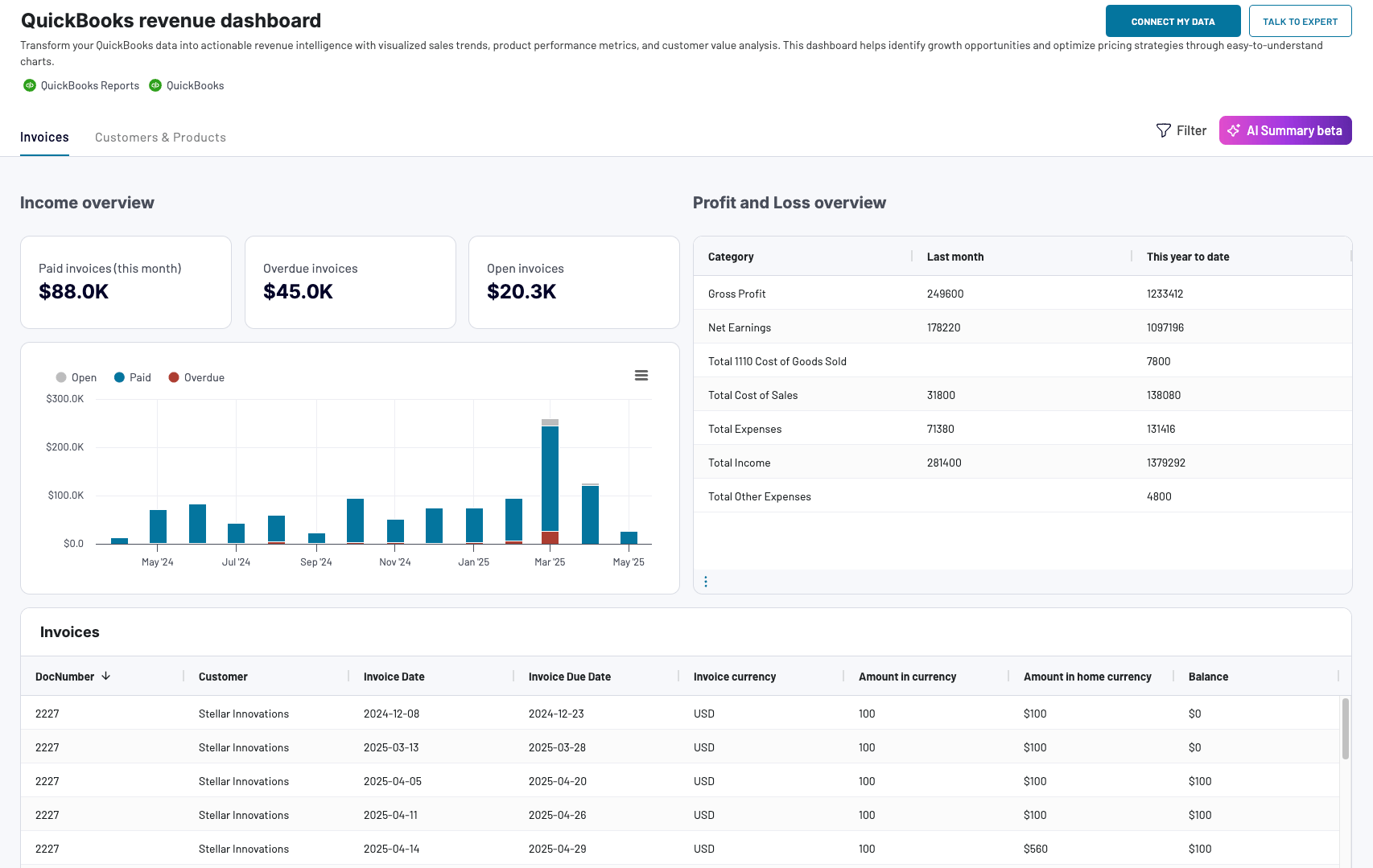

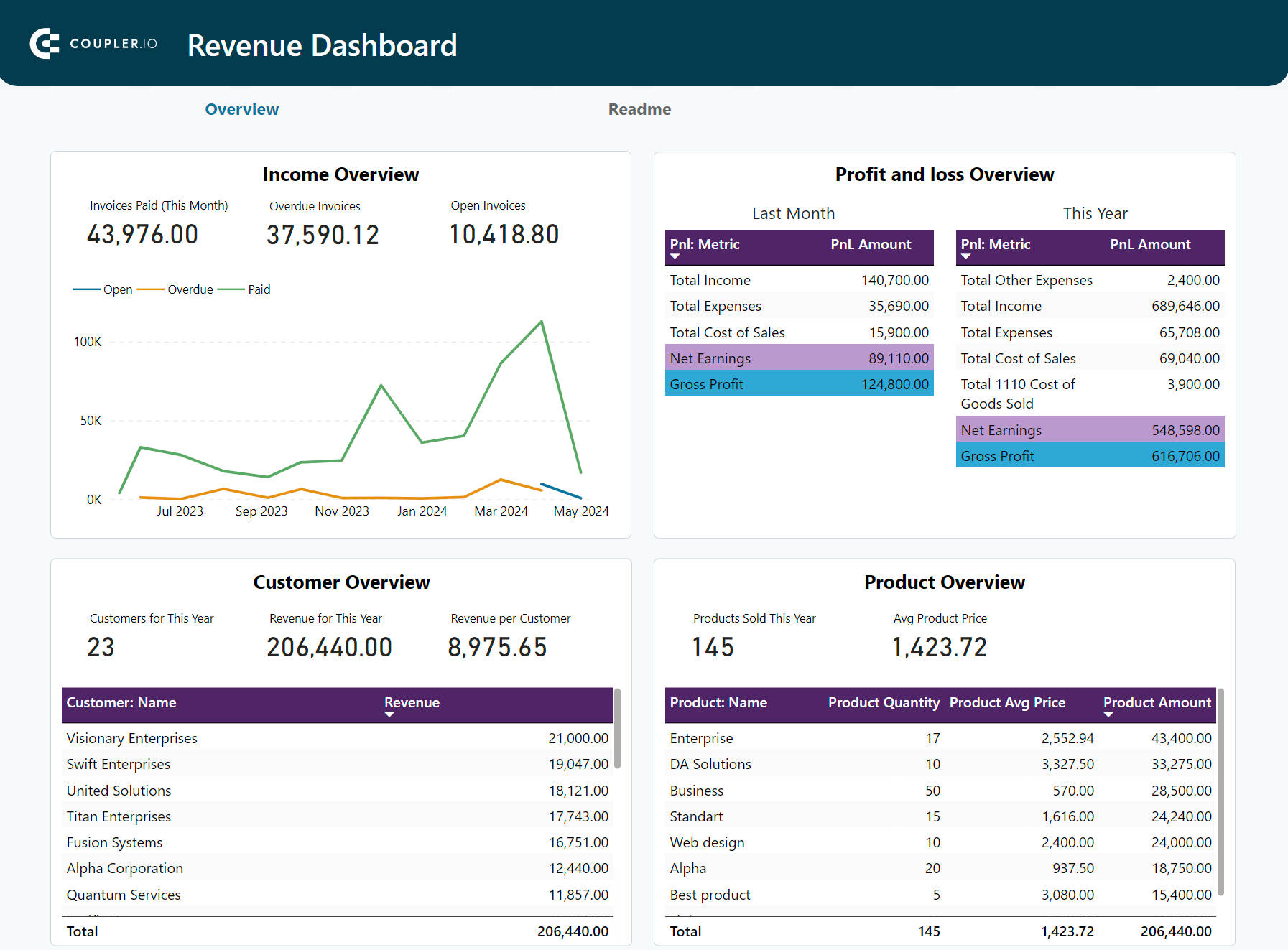

QuickBooks revenue dashboard

The QuickBooks revenue dashboard helps business owners and accountants track income, top-paying customers, best-selling products, and revenue trends. It eliminates the need for manual reporting by providing real-time revenue insights.

QuickBooks revenue dashboard + AI insights

QuickBooks revenue dashboard + AI insights

Preview dashboardWith this dashboard, you can:

- Monitor income trends: Tracks revenue fluctuations over 12 months, helping businesses spot seasonal changes and growth patterns.

- Analyze profit & loss: Compares revenue vs. expenses to assess overall profitability and cash flow health.

- Identify top customers: Highlights the highest revenue-generating customers to help businesses focus on retention and upselling.

- Track best-selling products: Provides insights into which products/services generate the most revenue, helping with pricing and inventory decisions.

The dashboard is available in the Coupler.io UI with faster performance and a built-in AI insights feature. At the same time, you can also use this profitability dashboard template for Looker Studio, Google Sheets, and Power BI. Connect your QuickBooks account via the Coupler.io connector and follow the Readme tab to use it with your data.

QuickBooks revenue dashboard

Transform your QuickBooks data into actionable revenue intelligence with visualized sales trends, product performance metrics, and customer value analysis. This dashboard helps identify growth opportunities and optimize pricing strategies through easy-to-understand charts.

QuickBooks revenue dashboard in Google Sheets

Analyze your revenue through a set of reports collected from QuickBooks Online on a single dashboard.

QuickBooks revenue dashboard in Looker Studio

Get an overview of your revenue based on the data from QuickBooks and unlock in-depth insights to drive informed business decisions.

QuickBooks revenue dashboard in Power BI

Monitor your income and expenses on an all-in-one revenue dashboard connected to your QuickBooks Online account.

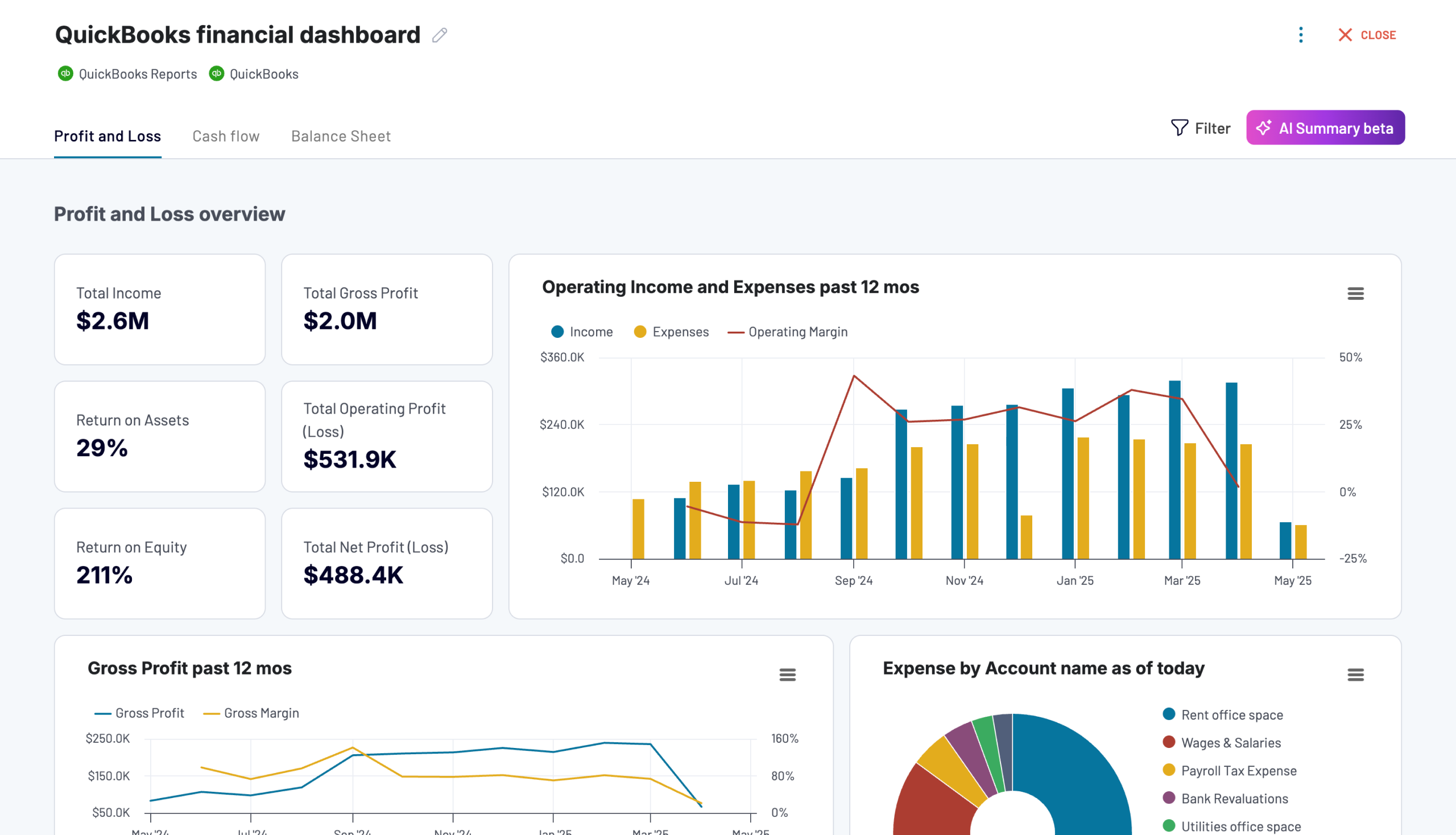

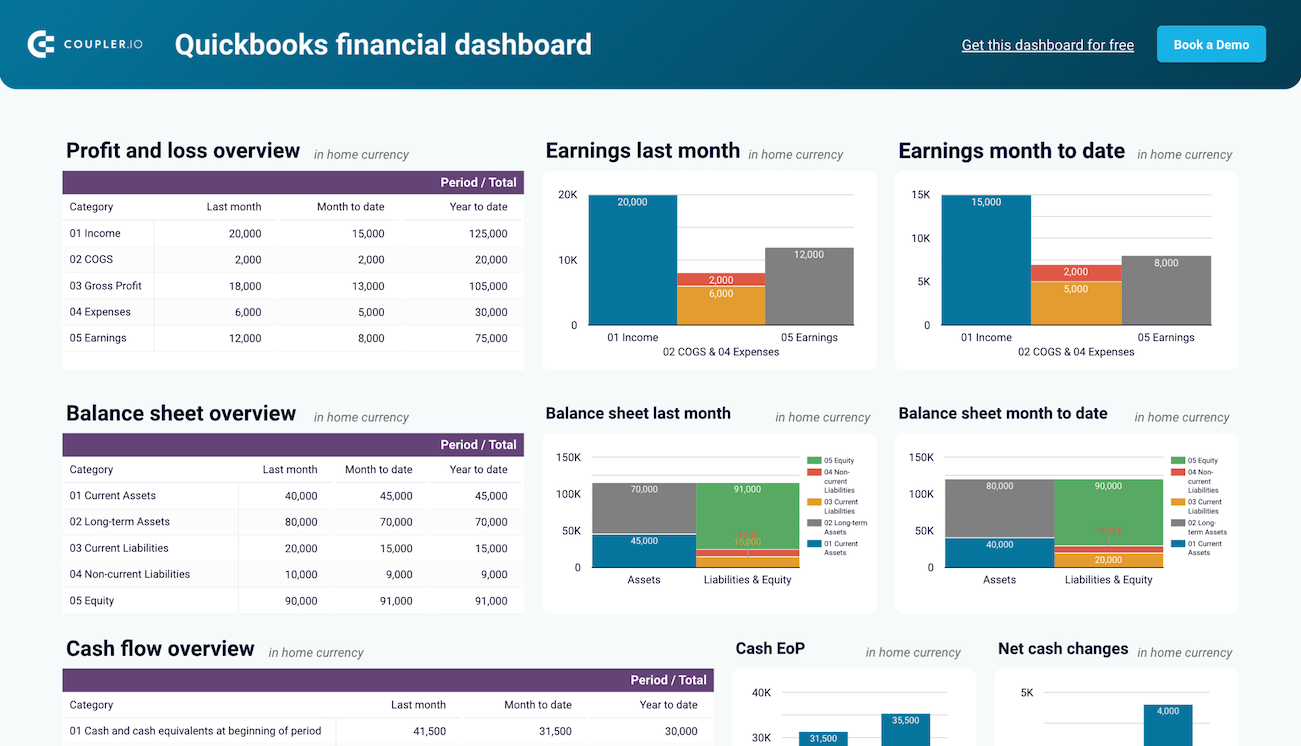

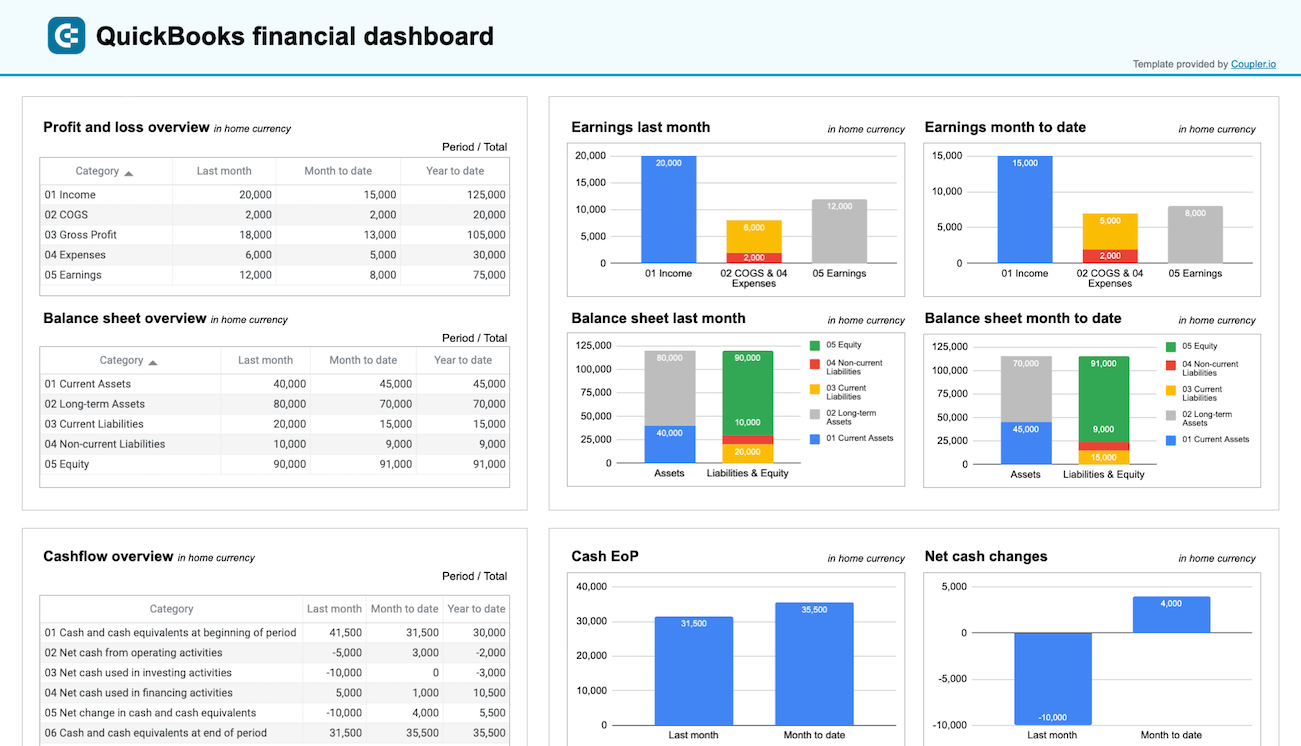

QuickBooks financial dashboard

The QuickBooks financial dashboard provides a real-time, at-a-glance view of a company’s earnings, balance sheet, and cash flow. It enables business owners and accountants to track financial performance without the need to manually compile reports.

With this CFO dashboard, you can:

- Analyze profit & loss trends: Breaks down income, cost of goods sold (COGS), expense reports, and net earnings for the last month, month-to-date, and year-to-date.

- Monitor the balance sheet: This tracks current assets, liabilities, long-term assets, and equity, ensuring businesses maintain financial stability.

- Track cash flow: Provides a clear picture of cash movements—opening balances, cash inflows and outflows, and cash equivalents at the end of the period.

- Monitor bank & cash accounts: Displays balances across different accounts and currencies to manage liquidity.

You can use this Coupler.io dashboard right in the tool or as a template in Looker Studio and Google Sheets. Simply connect your QuickBooks account using the Coupler.io connector and follow the steps in the Readme tab to populate the dashboard with your data.

QuickBooks financial dashboard

Tracks earnings, monitor cash flow, and analyze balance sheet changes with a dedicated dashboard that provides a clear picture of your business finances.

QuickBooks financial dashboard in Looker Studio

Monitor and analyze your business’s financial health with real-time insights into profit and loss, balance sheet, cash flow, and bank & cash accounts.

QuickBooks financial dashboard in Google Sheets

Get a clear snapshot of your business finances, including cash flow, P&L, balance sheets, and bank accounts, powered by data from QuickBooks Online.

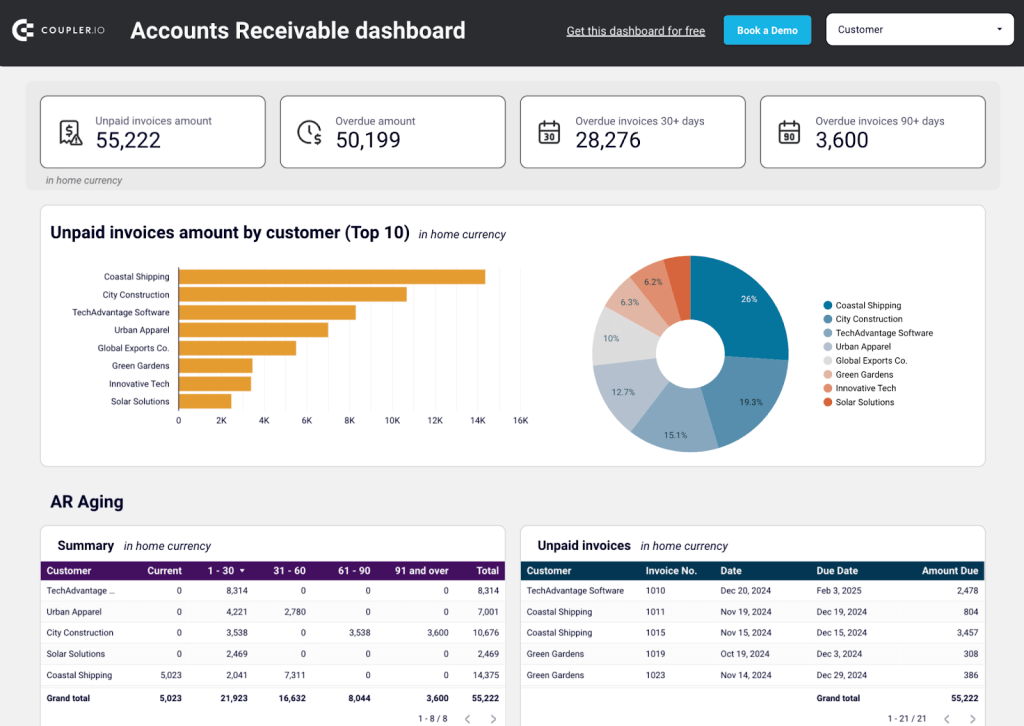

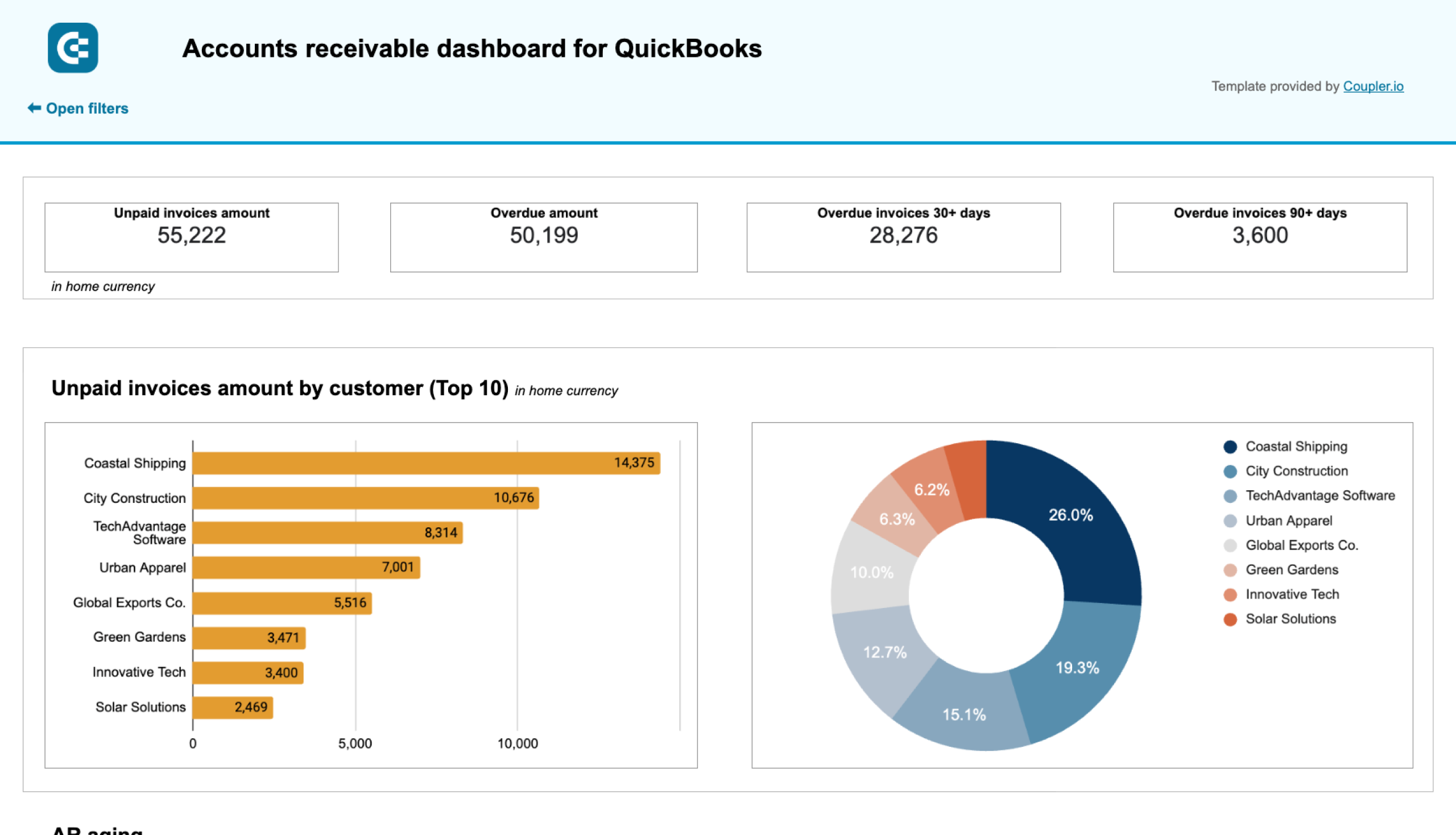

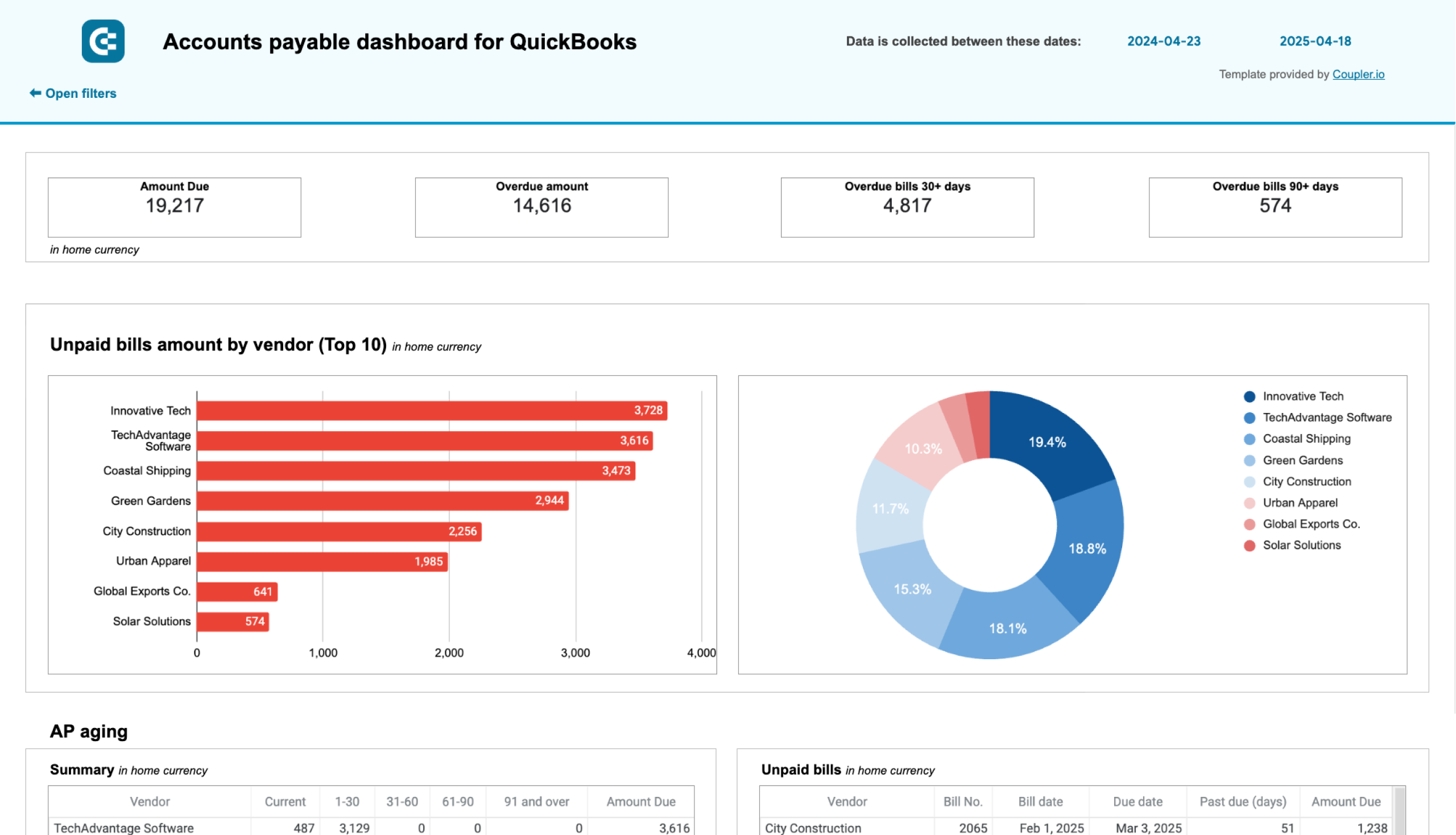

Accounts receivable dashboard for QuickBooks

The QuickBooks accounts receivable dashboard gives a complete overview of overdue payments, outstanding invoices, and customer payment behavior.

With this dashboard, you can track:

- Total unpaid invoices: See a breakdown of overdue amounts by different time periods (30, 60, 90+ days).

- Customer-wise payment status: Identify top overdue accounts and track their outstanding balances.

- Aging report insights: Monitor overdue invoices and assess payment delays.

- Paid vs unpaid trends: Compare cash inflows over different months to identify collection patterns.

- Invoice details: Get a clear snapshot of all customer invoices from the past year.

To integrate your data with this dashboard in Google Sheets or Looker Studio, use the Coupler.io connector and follow the instructions in the Readme tab.

Accounts receivable dashboard for QuickBooks in Google Sheets

Monitor customer payment statuses, overdue invoices, and collection trends with this dashboard connected to QuickBooks. Get clear visibility into your cash flow cycle with aging analysis and customer payment patterns to improve financial forecasting.

Accounts receivable dashboard for QuickBooks in Looker Studio

See which customers accumulate unpaid and overdue invoices, analyze AR aging, and track changes over time. Get useful insights for maintaining financial health.

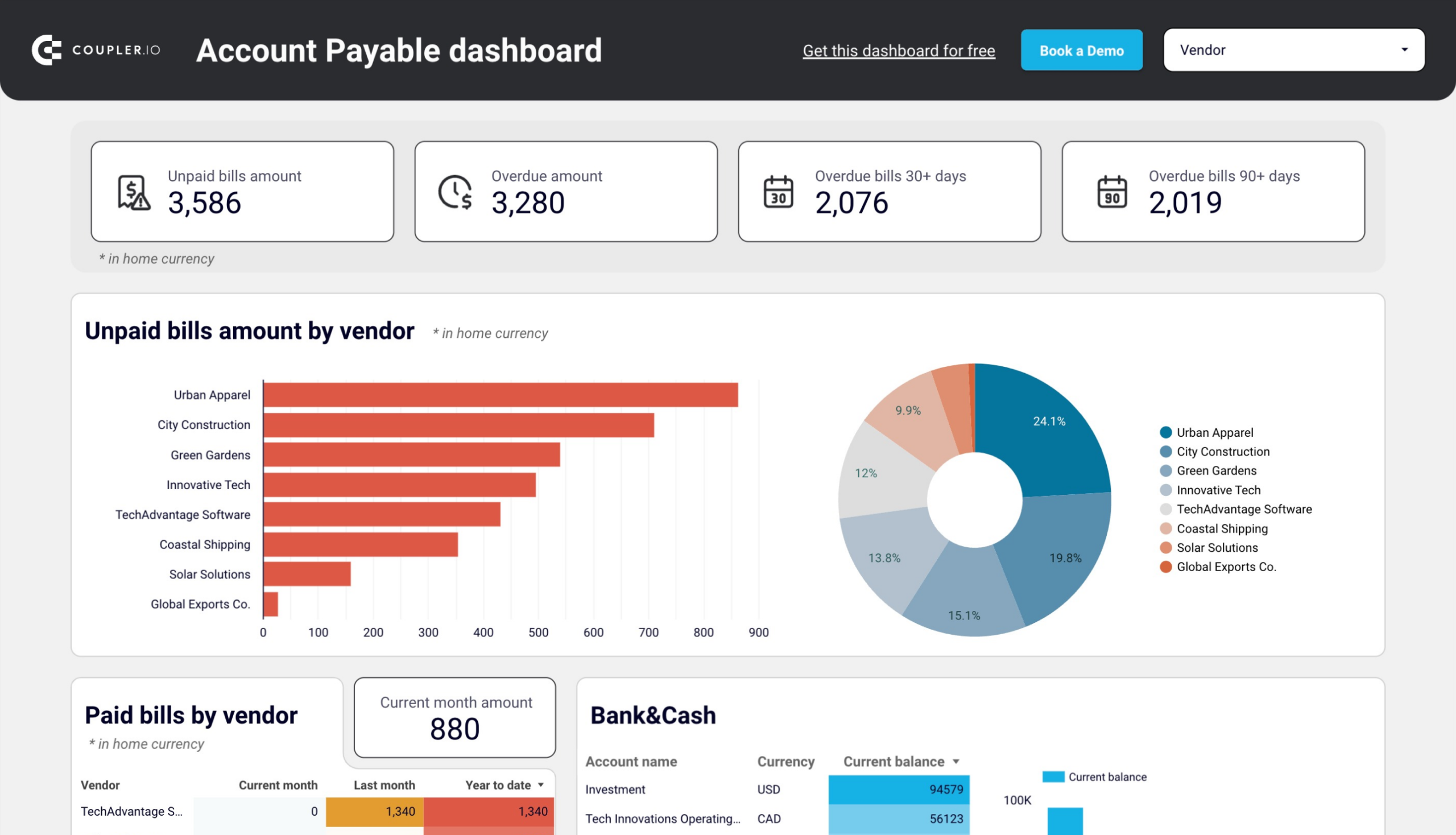

Accounts payable dashboard for QuickBooks

This dashboard simplifies vendor payment tracking by offering a real-time view of unpaid bills, due dates, and payment status. By displaying key insights in one place, it helps manage cash outflows effectively.

With this dashboard, you’ll get:

- Clear overview of unpaid bills: Get a snapshot of total outstanding amounts, overdue invoices, and upcoming payments.

- Vendor payment breakdown: Based on the overdue amount and due dates, Identify which suppliers need to be paid first.

- Aging report: Track overdue payments categorized by time frames (30, 60, and 90+ days) to avoid late fees.

- Bank & cash position: Compare outstanding bills with available cash reserves to plan payments efficiently.

- Historical vendor payments: Analyze previous payments by vendor to predict future cash needs.

The QuickBooks accounts payable dashboard is available in Google Sheets and Looker Studio. To integrate this dashboard with your data, simply connect your QuickBooks account using the Coupler.io connector and follow the instructions in the Readme tab.

Accounts payable dashboard for QuickBooks in Google Sheets

Track outstanding vendor obligations, payment schedules, and expense patterns with data from QuickBooks. This dashboard helps you manage cash flow, identify payment priorities, and maintain healthy supplier relationships through visualized aging reports.

Accounts payable dashboard for QuickBooks in Looker Studio

Get an overview of unpaid, overdue, and paid bills grouped by vendor. The dashboard helps you prioritize payments and improve cash flow management.

Harvest time-tracking dashboard

Harvest’s time-tracking dashboard makes managing employee hours easier. It compiles billable hours, project time distribution, and workforce activity in one place, making it helpful in monitoring productivity trends and improving payroll accuracy.

With this dashboard, you’ll have:

- Accurate billable tracking: Capture logged hours for projects and client invoicing without manual input.

- Performance evaluation: Identify workload imbalances to prevent overworked employees or idle resources.

- Flexible filtering: Sort by team member, project, or task for granular time analysis.

- Calendar-based visualization: Detect trends, unusual work hours, or gaps in reported time.

This dashboard is available in Looker Studio and Power BI. You can set it up with your data by using the Coupler.io connector and following the instructions in the Readme tab.

Clockify time-tracking dashboard

For businesses using Clockify, this dashboard ensures accurate work-hour tracking, project time breakdown, and productivity assessments to make payroll calculations easily.

With this dashboard, you’ll have:

- Real-time timesheet updates: Track how work hours fluctuate across projects and employees.

- Productivity analysis: Monitor billable vs. non-billable hours to refine efficiency strategies.

- Custom data views: Filter reports by client, task, or individual team members for targeted insights.

- Visual trend analysis: Use charts and calendar views to identify irregular time logs or burnout risks.

Built for Looker Studio and Google Sheets, this dashboard integrates with Clockify using the Coupler.io connector. To populate the dashboard with your data, follow the instructions in the Readme tab.

Benefits of accounting automation

- No manual work: Manually entering financial information is time-consuming and prone to mistakes. Automation allows businesses to sync transactions directly from their bank accounts, invoicing systems, or payroll software.

For example, QuickBooks automation can track sales transactions for your e-commerce store, reducing data-entry errors by up to 80% and saving your team over 10 hours per week in bookkeeping tasks.

- Cuts operational costs: Hiring extra accountants for routine bookkeeping increases costs. Automated systems handle tax calculations, payroll processing, and invoice tracking without additional staff.

For example, by automating bookkeeping and payroll using an all-in-one accounting tool, your business can reduce staffing needs and potentially save up to $40,000 annually. This is equivalent to the cost of hiring a full-time bookkeeper.

- Prevents errors: Miscalculated payroll, duplicate invoices, or incorrect tax filings can lead to financial losses. Automated accounting software applies validation checks and rule-based processing to minimize errors.

For example, by automating payroll with dedicated payroll software, your business can significantly reduce payroll errors—potentially by up to 95%. This helps avoid costly fines and tax penalties, potentially saving thousands of dollars each year.

- Scales with business growth: As a company grows, its financial data multiplies, making manual tracking impractical. Accounting tools like NetSuite process high transaction volumes without increasing workload.

For example, if your retail business is expanding rapidly, accounting automation tools like NetSuite can efficiently manage increased sales and expense tracking. This could free up over 20 hours per week for your accounting team.

- Better decision-making: With access to real-time financial insights, businesses can plan strategically. Automated dashboards help monitor revenue trends, identify spending patterns, and adjust budgets accordingly.

For example, using automated financial dashboards, your business can quickly spot rising raw material costs like an unexpected 15% increase. This allows you to renegotiate supplier contracts early and save significant expenses annually.

- Saves time on reporting: Generating financial reports manually can take days. Automated reporting tools pull data from multiple sources to create instant statements.

For example, by connecting QuickBooks and Stripe with Coupler.io, your digital marketing agency can automate monthly accounting reporting. This can potentially reduce reporting time from over 15 hours per month to just minutes, boosting efficiency by up to 90%.

Accounting automation trends shaping the future

Accounting is no longer just about balancing books. It is evolving into a data-driven, intelligent system that helps you make strategic decisions in real-time. With vast amounts of data (~ 402.74 million TB every day), you can use automation to eliminate inefficiencies, prevent fraud, and improve financial forecasting.

But what exactly is driving this shift in accounting? Let’s explore the biggest trends shaping the future of accounting automation.

AI and machine learning in automation

Accounting is shifting from reactive number-crunching to proactive financial intelligence—and artificial intelligence (AI) is at the heart of this transformation.

Imagine a world where bookkeeping updates itself, errors are flagged before they cost you money, and financial reports predict your next move. That future is already here!

The AI in the accounting market is projected to grow from $6.68 billion in 2025 to $37.60 billion by 2030. This is a sign that businesses are moving toward AI-driven financial systems.

- Automated data entry and processing: AI extracts data from invoices, receipts, and bank statements and categorizes transactions without human input. Tools like Dext and AutoEntry save 80% of the time spent entering invoice data manually.

- Fraud detection and anomaly recognition: Machine learning analyzes financial transactions and flags sophisticated fraud attempts that human oversight or basic systems might miss. For example, AI can identify round-dollar fraud, where a company’s books contain an unusual number of transactions rounded to the nearest hundred or thousand which is often a sign of financial manipulation.

- Predictive cash flow and financial forecasting: AI cross-checks bank transactions with accounting records to catch mismatches instantly. It can flag a payment recorded for ?50,000 instead of ?500,000 to prevent costly reporting errors.

- Automated reconciliation and error detection: It analyzes past spending and revenue trends to predict when a business might encounter cash flow issues. For example, an AI-powered system warns a SaaS company based on the current burn rate that it will run out of cash in 90 days. This will help to adjust expenses or seek funding.

Blockchain for transparency

Accounting relies on trust, but fraud, tampering, and human errors can put financial integrity at risk. Blockchain creates a tamper-proof, decentralized ledger that keeps financial records secure, transparent, and verifiable in real time.

- Tamper-proof financial records: Every transaction recorded on a blockchain is immutable—it cannot be altered or deleted, reducing the risk of fraudulent edits. If a company uses blockchain-based invoicing, then once a payment record is logged, it cannot be modified to hide discrepancies.

- Instant auditing and compliance: Auditors no longer need to manually verify records. Blockchain provides a real-time, transparent transaction history, saving auditing time. A multinational company implementing blockchain can allow auditors to instantly access financial data without retrieving files from multiple accounting departments.

- Smart contracts for automated payments: Blockchain enables self-executing contracts that process payments automatically when conditions are met. This removes delays and prevents disputes. A supplier receives payment automatically once a shipment is delivered and verified without manual approvals.

- Fraud detection and prevention: Blockchain prevents double spending and duplicate transactions, which are common issues in traditional systems. A business can prevent invoice fraud by ensuring the same invoice cannot be submitted multiple times under different account numbers.

Advanced data analytics

Traditional accounting reports give you a snapshot of past financials. But they don’t always reveal why numbers are changing or what to expect next. With advanced data analytics, businesses can move beyond static reports to uncover patterns, predict risks, and make proactive financial decisions.

- Identifying cost trends: Businesses can analyze historical spending patterns to spot rising costs before they impact profits. For instance, a manufacturing firm tracks raw material costs and identifies a steady increase in steel prices. They negotiate supplier contracts early, saving 5% on bulk orders.

- Real-time budget adjustments: Instead of setting fixed annual budgets, businesses can adjust spending dynamically based on real-time data. For example, a marketing agency detects underspending in ad campaigns and reallocates funds to higher-performing ads to increase ROI.

- Scenario planning for financial decisions: Companies can simulate different financial outcomes based on ‘what-if’ scenarios before making major decisions. For instance, a SaaS company evaluates how a 10% increase in customer churn would impact cash flow and adjusts retention strategies accordingly.

- Automated reporting for faster insights: Instead of waiting for monthly reports, businesses can access live financial dashboards with up-to-date metrics. For example, a CFO using a self-updating financial dashboard in Power BI can track revenue growth and adjust sales strategies based on real-time data.

Accounting automation risks & how to mitigate them

Automation improves efficiency, but it also comes with risks.

If not appropriately managed, businesses may face security threats, integration failures, or compliance issues. Here’s how to identify and mitigate these risks effectively:

Data security vulnerabilities

Storing financial data in cloud-based systems increases the risk of cyberattacks, unauthorized access, and data breaches. A single vulnerability can expose sensitive financial records, leading to fraud, financial loss, and legal consequences.

How to mitigate?

- Enable multi-factor authentication (MFA): Require additional verification (e.g., OTP, biometric authentication) for all automated accounting system logins.

- Use encryption: Encrypt data both in transit and at rest so that even if hackers access it, they cannot read or misuse it.

- Conduct regular security audits: Review access logs, identify unusual activities, and patch vulnerabilities before they can be exploited.

Over-reliance on automation

Automated systems process vast amounts of financial data but are not immune to errors. If businesses depend entirely on automation, incorrect tax calculations, duplicate transactions, or misclassified expenses can go unnoticed.

How to mitigate?

- Implement human oversight: Assign finance teams to randomly audit automated reports and flag inconsistencies.

- Set up alerts for anomalies: Use AI-driven tools to detect unexpected transaction patterns and require manual approval for flagged cases.

- Test automation with small-scale business processes first: Before fully automating key accounting tasks, test with low-risk functions (e.g., recurring invoices) and review results manually.

Integration challenges

Accounting automation tools must integrate with ERP systems, banking platforms, and tax software. Compatibility issues can lead to data mismatches, failed imports, or duplicated journal entries.

How to mitigate?

- Choose tools with strong API capabilities: Platforms like Coupler.io, QuickBooks, and Xero provide reliable data syncing with other software.

- Test integrations before full deployment: Conduct a pilot run to ensure data flows correctly between systems before rolling out automation across all departments.

- Ensure IT and finance teams collaborate: Regular communication between IT and accounting teams helps to troubleshoot integration issues rapidly.

Regulatory compliance risks

Tax laws and financial regulations frequently change, and automation tools may not always update in real time. Relying on outdated tax rates or compliance policies can lead to penalties, audits, or incorrect financial filings.

How to mitigate?

- Use accounting software with automatic compliance updates: Tools like Avalara, Vertex, and TurboTax Business track tax regulation changes and update calculations accordingly.

- Conduct periodic audits: Even with automated compliance features, schedule internal audits to verify that financial records align with legal requirements.

- Consult regulatory experts: For complex tax and compliance matters, ensure your accounting team has access to legal and tax professionals.

Training and change management

Employees may resist automation due to a lack of familiarity, fear of job displacement, or difficulty adapting to new accounting workflows. Poor implementation can lead to underutilized software, errors in automation settings, or unnecessary delays.

How to mitigate?

- Provide hands-on training: Instead of generic training sessions, offer role-specific training customized for accountants, finance managers, and auditors.

- Maintain clear documentation: Create a knowledge base with step-by-step guides, video tutorials, and FAQs for troubleshooting automation issues.

- Offer continuous support: Assign a designated support team or automation lead to help employees adjust to new workflows and resolve concerns quickly.

The future of accounting after automation

Will accountants lose jobs?

This is the question of the decade in the accounting world.

With automation handling data entry, reconciliations, and reporting, it’s easy to assume accountants may become obsolete.

But automation isn’t replacing accountants—it’s redefining their role.

For years, accounting focused on recording transactions and balancing general ledgers. Now, with AI automating these manual tasks, accountants are shifting to strategy and advisory roles. Instead of merley matching transactions, they analyze cash flow trends, optimize tax planning, and guide financial decisions.

The future belongs to tech-savvy accountants who embrace AI, data analytics, and automation. Businesses will seek accounting professionals who don’t just record numbers but extract valuable insights from them. Those who adapt will thrive, leading finance teams with real-time data and predictive analytics.

Automation isn’t replacing accountants. It’s making them more valuable than ever.

The real question isn’t whether accounting jobs will disappear but who will leverage automation to stay ahead?

Automate accounting reporting with Coupler.io

Get started for free